It’s late August, earlier than a vacation weekend. You don’t want but one other evaluation of POTUS’ try to fireplace Lisa Cook dinner – there have been lots already.

As an alternative, let’s get philosophical. I wish to contemplate a special query: Why Aren’t Markets Freaking Out? Paul Krugman raised that query immediately, and whereas I don’t disagree along with his view, my framing could be very completely different.

Let’s begin with Benjamin Graham’s well-known aphorism that “Within the brief run, the market is a voting machine, however in the long term, it’s a weighing balance.” I might annotate1 Graham’s aphorism as follows:

Markets are likelihood machines.

Certain, folks “vote” with their {dollars}, however that’s a tautology, a definition that lacks any helpful context for understanding the market proper now.

Here’s a extra helpful framework:

1. The long run is inherently unknown (aka “No one is aware of something”)

2. Traders specific their expectations through their capital

3. Collectively, this kinds a market consensus.

Let’s flesh this out a bit extra:

No one is aware of something signifies that none of us know, with any diploma of certainty, how any of the present points will ultimately resolve. Cook dinner’s (alleged) firing, tariffs2, inflation, company earnings, no matter. We are able to analyze, estimate, extrapolate, and hypothesize, however we merely don’t know exactly what the result might be – but.

However we are able to (and do) specific our particular person views by allocating our capital. We kind a perspective, think about a potential future consequence, maybe establish relative asymmetries. We make a threat/reward evaluation after which put our money to work. The short-term votes Graham was referring to have been these greenback investments. Collectively,that is how a market consensus is fashioned. Typically, the best likelihood consequence seems to be proper – all-time highs hold going increased! And different occasions, the best likelihood consequence is unsuitable – Decrease yields! Recession! Fed cuts!

Earlier than we all know the market consequence of any subject, now we have solely an array of chances, collectively decided, as to what may occur.

~~~

Contemplate an excerpt from James Surowiecki’s “The Knowledge of Crowds.” It discusses the January 28, 1986, Challenger house shuttle catastrophe. Right here is the half I’m most intrigued by:

“Inside minutes, buyers began dumping the shares of the 4 main contractors who had participated within the Challenger launch: Rockwell Worldwide, which constructed the shuttle and its primary engines; Lockheed, which managed floor help; Martin Marietta, which manufactured the ship’s exterior gasoline tank; and Morton Thiokol, which constructed the solid-fuel booster rocket.”

On the finish of that day (1/28/86), the primary three shares have been off solely 3%, however Morton Thiokol’s inventory closed down 12%. Folks have interpreted this as a “Knowledge of Crowds” phenomenon; some declare this as proof that merchants had by some means deduced that the disaster was Morton Thiokol’s fault; or that markets found out that their booster rocket O-rings have been finally responsible for the explosion.

I encourage to vary.

The market didn’t and couldn’t “know” that.

Somewhat, buyers made a probabilistic evaluation as to what would happen to any of these 4 firms’ earnings and inventory costs if any (or some mixture) have been the one(s) at fault. This was a probabilistic evaluation of the influence on every firm.

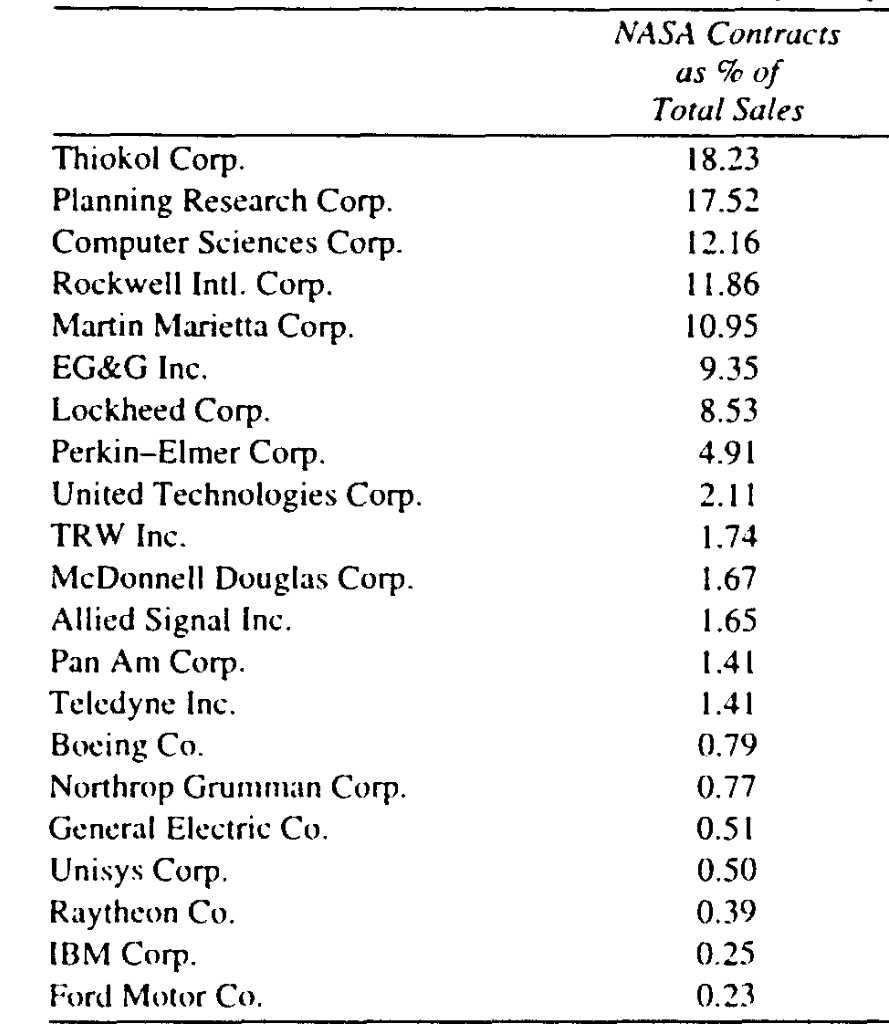

Rockwell ($8B market cap) had US aerospace, automotive, and industrial know-how companies; Lockheed ($2.5B) was an unlimited protection contractor; Martin Marietta ($3B) held aerospace, protection, electronics, know-how, aluminum, development supplies, and chemical substances companies. (Lockheed and Martin Marietta merged in 1995 to kind the world’s largest protection contractor).

Rockwell ($8B market cap) had US aerospace, automotive, and industrial know-how companies; Lockheed ($2.5B) was an unlimited protection contractor; Martin Marietta ($3B) held aerospace, protection, electronics, know-how, aluminum, development supplies, and chemical substances companies. (Lockheed and Martin Marietta merged in 1995 to kind the world’s largest protection contractor).

The smallest and least diversified entity was Morton Thiokol ($1.7B). It held Morton Salt, different chemical makers, and constructed rockets. That they had the best publicity to the aerospace trade. NASA contracts as a share of Thiokol’s gross sales have been over 18%; Rockwell was lower than 12%; Martin Marietta was lower than 11%; Lockheed was 8.5%. If any of those 4 firms had been discovered to be at fault, it might have been most impactful to Morton Thiokol. They have been, because the New York Instances reported, the corporate with “probably the most to lose when it comes to earnings” as a result of catastrophe.

That likelihood is what the markets had decided — not which firm was at fault.

~~~

Why are markets not freaking out? As a result of the best likelihood case (for now) is that earnings and revenues stay excessive, the financial system stays strong, a Fed reduce is forthcoming, and all of this noisy political stuff will finally work out ultimately.

You may criticize market chances as a mash-up of wishful considering and clever evaluation. There are occasions, with the advantage of hindsight, when what seemed like market insanity was really rational – if solely we knew then what we all know now. Therefore, the likelihood machine is laying out numerous potential outcomes, together with costs that roughly mirror these outcomes accordingly.

The dispersion of outcomes features a full vary of potentialities. Typically, these are very completely different, even reverse, contradictory outcomes. There are occasions when markets look like failing to acknowledge particular dangers. Little doubt, there have been occasions when that was true. However we additionally want to simply accept that at different occasions, markets merely have no idea.

Making probabilistic bets on very particular events involving folks, coverage, and politics is “squishy.” There’s additionally an enormous distinction between assessing the chance of a White Home takeover of the Fed, and understanding what its influence on costs might be sooner or later. We merely have no idea…

~~~

For these of you who do wish to discover the Fed independence subject, I direct your consideration to Jon Hilsenrath’s August 8th commentary, “The Fourth Seat.” Jon spent 25 years on the WSJ as a reporter and editor, and for a protracted whereas, was the Journal’s major Fed Whisperer.

He was early in explaining the mechanics of any White Home energy seize of the Fed:

“The President is presently lined as much as have three sympathetic voices on the Fed’s seven-member board subsequent yr: Governors Chris Waller and Michelle Bowman, whom he appointed throughout his first time period, and a 3rd seat he’s now filling with Miran and later probably by the brand new chairman.

It’s a seven-member board. If Powell vacates his seat as a governor when his chairmanship ends subsequent yr, he’s probably handing Trump a decisive, extremely disruptive vote on the Fed board.

With 4 votes, the Washington-based board has the authority to fireplace Fed regional financial institution presidents and reconstitute their boards of administrators. Discord on the Fed is coming for the regional banks and this may be the mechanism.”

That’s nearly as good a proof of the current circumstances as any you may learn.

Within the meantime, I’m watching as Mr. Market tries to suss out the varied potential and possible outcomes…

See additionally:

Why Aren’t Markets Freaking Out? (Paul Krugman, Aug 28, 2025)

Why the bond market stays so calm amid Trump’s Fed struggle. (Axios, Aug 28, 2025)

Beforehand:

Would possibly Tariffs Get “Overturned”? (July 31, 2025)

Perhaps Mr. Market Is Rational After All (August 7, 2020)

Embrace Your Inside Statistician! (March 18, 2011)

The kinda-eventually-sorta-mostly-almost Environment friendly Market Concept (November 20, 2004)

No one Is aware of Something (full archive)

__________

1. My full annotation:

“Within the brief run, the market is a likelihood machine, however in the long term, it’s a knowledge multiplied by psychology machine.”

2. What are the chances that Tariffs get overturned? Extra on this coming subsequent week…