Q.

I’m a 58-year-old surgical nurse retiring in July. My

might be roughly $55,000 yearly and it’ll begin paying out in September. I’ve $48,000 in unused

registered retirement financial savings plan

(RRSP) contribution room. Ought to I

on my 2025 taxes? I’ve sufficient saved to take action. Or, ought to I persist with topping up my

tax-free financial savings account

(TFSA)?

—Thanks, Richard in Ontario

FP Solutions:

Richard, there are some things to contemplate when deciding on an RRSP or TFSA contribution. The very best place to start out is with understanding of the maths behind RRSPs and TFSAs.

It’s usually stated that RRSP contributions are made with pre-tax cash and TFSA contributions with after-tax cash. Though true by design, it isn’t true based mostly on the best way most individuals make RRSP contributions.

Most individuals assume, “I’ve $10,000, ought to I add it to my RRSP or TFSA?” If you’re including to your RRSP you’ll doubtless do it in certainly one of 3 ways: you’ll gross up the quantity (which I’ll clarify later), you’ll reinvest the tax refund, or you’ll make investments solely the $10,000.

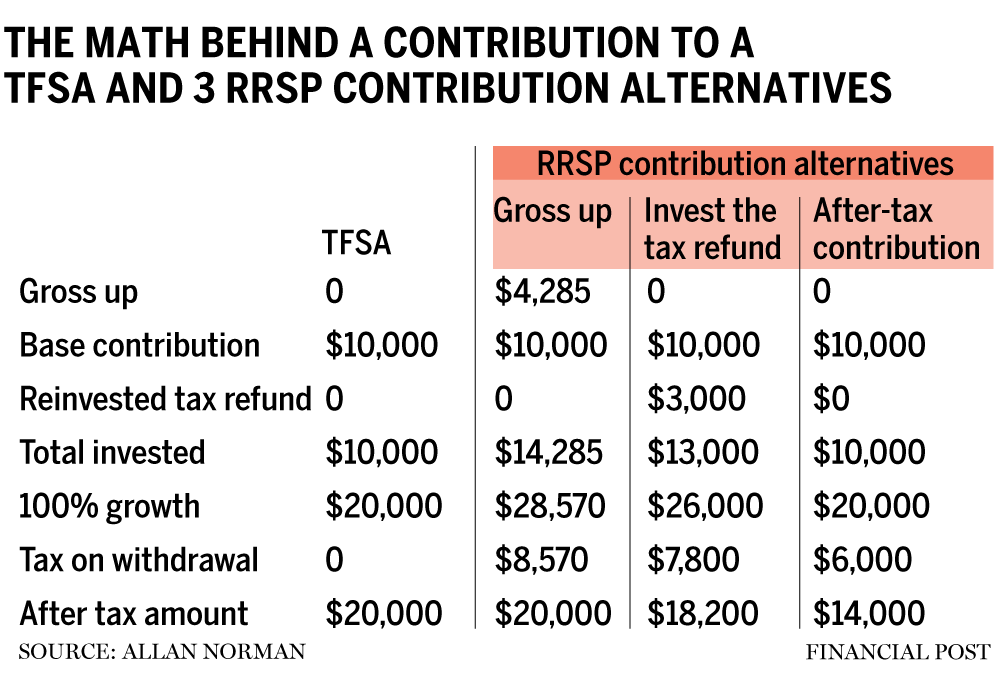

The accompanying desk illustrates the maths behind a $10,000 contribution to a TFSA, and three RRSP contribution options. I’m assuming the total contribution and withdrawal is taxed at 30 per cent and the preliminary funding grows by 100 per cent over time.

The ends in the chart are displaying no distinction between TFSAs and RRSPs if you’re grossing up (pre-tax) your RRSP contribution. It’s also possible to infer that if on the time of withdrawal you might be in a decrease tax bracket, the RRSP beats the TFSA and if in a better tax bracket, the TFSA beats the grossed-up RRSP.

Additionally obvious from the desk is that if you’re not grossing up your RRSP contribution the maths favours a TFSA contribution.

Grossing up your RRSP contribution means contributing an quantity equal to what you needed to earn earlier than tax, to have $10,000 in your checking account. Right here is the gross up system: $10,000/(1-30 per cent (your marginal tax charge)). To get the additional $4,285 you may both borrow the cash from a lender or from your self after which pay it again whenever you get your tax refund.

Richard, you could be questioning, for those who maximize your $48,000 RRSP contribution how will you gross up your contribution? You’ll be able to’t, however it’s nonetheless vital to grasp the maths behind contributions. It is advisable even be wanting on the different advantages of constructing RRSP contributions.

RRSPs and TFSAs are each tax shelters. Nonetheless, you’ll doubtless cease incomes RRSP contribution room when you cease working, whereas every year you’ll earn extra TFSA contribution room. Plus, this can be your highest revenue incomes 12 months. Primarily based on that it could be finest to maximise your RRSP after which use the tax refund to high up your TFSA.

Needless to say you don’t have to assert all or any of your RRSP tax deduction within the 12 months you make an RRSP contribution. Your revenue in 2025 might be made up of wage and pension and could also be your highest incomes 12 months till you begin your

(CPP) and

(OAS). You might need to declare an RRSP deduction to deliver your revenue all the way down to the highest of the primary tax bracket and save your remaining RRSP deduction for a future 12 months or years. In case you resolve to do some part-time work the saved RRSP deductions could also be helpful.

One other consideration is that cash inside an RRSP compounds tax-free. The cash you’ve saved to make the $48,000 contribution could also be incomes taxable curiosity, dividends, or capital good points. The longer you’ve the cash in your RRSP the larger this benefit turns into. Now, if you’re planning to spend the $48,000 within the subsequent 12 months or two you could solely need to add sufficient to your RRSP to deliver you all the way down to the highest of the decrease tax bracket — about your pension revenue — after which high up your TFSA with the remainder, presumably leaving some non-registered cash.

Richard, as I discussed earlier, RRSPs and TFSAs are each tax shelters and RRSPs have a restricted shelf life in contrast with TFSAs. If that is long-term cash you’ve saved so as to add to your RRSP it could be finest to make use of it when you have the upper revenue and save your TFSA room.

Allan Norman, M.Sc., CFP, CIM, gives fee-only licensed monetary planning providers and insurance coverage merchandise by Atlantis Monetary Inc. and gives funding advisory providers by Aligned Capital Companions Inc., which is regulated by the Canadian Funding Regulatory Group. He may be reached at alnorman@atlantisfinancial.ca.

Bookmark our web site and help our journalism: Don’t miss the enterprise information it’s worthwhile to know — add financialpost.com to your bookmarks and join our newsletters right here.