Final evening (March 25, 2025), the Australian authorities delivered the most recent fiscal assertion for 2025-26 (aka – The Funds – and, in doing so tried to win renewed electoral attraction given its waning recognition and a nationwide election that must be held within the subsequent 6 or so weeks. So it provided the tax cuts and different inducements to the voters. However the underlying tenor of the fiscal place is unsustainable not as a result of it’s predicting on-going fiscal deficits out to 2028-19 however as a result of these deficits will likely be too small relative to different tendencies which are more likely to happen (exterior sector and family consumption spending). Whereas the commentariat has been in conniptions about ‘eye watering pink ink’ for a far as we will see (their eyes are poor), the actual fact is that the projected fiscal deficit is in regards to the common degree since 1970-71. However within the present setting, the forecasted authorities contraction will harm the financial system and push unemployment up additional than they’re forecasting. Positive sufficient, the Authorities handed out some dollops of cost-of-living aid to low-income households – a couple of pennies within the scheme of issues and that can most likely assist them retain votes. Bu with all of the challenges forward now will not be the time to be in contractionary mode. Successful the election is one factor, however neglecting a bunch of existential issues within the medium time period will not be the way in which to go.

Authorities erases the unemployed from the general public debate

In ‘Funds Paper No.1’, Assertion 2: Financial Outlook, we observe the next forecasts.

| Combination | 2023-24 (Precise) | 2024-25 | 2025-26 | 2026-27 |

| GDP progress | 1.4 | 1.5 | 2.25 | 2.5 |

| Present Account (% of GDP) | -1.3 | -1.75 | -3.75 | -4.25 |

| Public Remaining Demand | >4.23 | 5.0 | 3.0 | 2.0 |

| Employment | 2.2 | 2.75 | 1.0 | 1.25 |

| Unemployment | 4.0 | 4.25 | 4.25 | 4.25 |

| Participation charge | 66.8 | 67.25 | 67.0 | 66.75 |

| Inflation | 3.8 | 2.5 | 3.0 | 2.5 |

The most recent ABS estimates point out that inhabitants progress “grew by 1.8 per cent within the 12 months main as much as 30 September 2024” (Supply).

The Treasury forecasts that participation will likely be largely steady (slight decline).

Word additionally that the implied productiveness progress within the above forecasts (GDP progress minus Employment progress) is round 1.25 per cent by the tip of the forecast interval.

The one motive that employment progress is initially robust then falling away is as a result of productiveness progress is assumed to be adverse in 2024-25 earlier than bettering to 1.25 per cent within the final two years of the forecast interval.

How does that affect the unemployment charge forecasts?

The well-known US economist Arthur Okun developed a rule of thumb about the way in which unemployment reacts to GDP progress.

The rule of thumb has it that if the unemployment charge is to stay fixed, the speed of actual output (GDP) progress should equal the speed of progress within the labour drive plus the expansion charge in labour productiveness.

Keep in mind that labour productiveness progress reduces the necessity for labour for a given actual GDP progress charge whereas labour drive progress provides employees that need to be accommodated for by the true GDP progress (for a given productiveness progress charge).

If we assume the labour drive grows in step with the assumed underlying inhabitants forecasts – so round 1.8 per cent (given participation is estimated to be steady) and productiveness progress is round 1.25 per cent, then GDP progress must be 3.05 per cent in every of the forecast years if the unemployment charge is to remain unchanged.

A cursory have a look at the Desk above, exhibits the next if the forecasts transform truth:

1. 2024-25 – GDP will likely be above the required charge by round 0.95 factors as a result of productiveness progress is assumed to be adverse.

2. 2025-26 – GDP will likely be under the required charge by round 0.8 factors.

3. 2026-27 – GDP progress will likely be under the required charge by round 0.55 factors..

The implication is that it’s exhausting to see how the unemployment charge enhance may be confined to a forecast 0.25 factors over the forecast interval.

The rule of thumb tells us that it’ll rise by round 0.4 factors over the forecast interval..

That’s clearly an approximation.

However it suggests there’s not consistency throughout the modelled forecasts utilized by Treasury.

The one means that the unemployment charge enhance may very well be confined to 0.25 factors over the following three years is that if productiveness progress stayed low or adverse.

The opposite means of contemplating that is to simulate the underlying labour drive aggregates primarily based on the Treasury assumptions with respect to employment progress.

That simulation (utilizing the ABS inhabitants progress information) and the Treasury employment progress forecasts, delivers an unemployment charge of 5.03 per cent by the tip of June 2027 with unemployment rising from 612.6 thousand in February 2025 to 794.3 thousand by the tip of June 2027.

Keep in mind that the Treasury forecasts are for fiscal years so a rising unemployment charge will document a decrease annual common than its endpoint within the month of June 2027.

My greatest guess is that the unemployment charge will rise nearer to five per cent than 4.25 per cent as estimated by the Treasury.

It tells me that the fiscal place the federal government is selecting as its coverage technique is just too contractionary.

Additional, I’ve commonly indicated that the unemployed are pressured to stay on so-called Jobseeker advantages (unemployment advantages) that are more and more under the recorded poverty line.

Successive federal governments have refused to handle that rising hole.

In final evening’s fiscal assertion, the Authorities didn’t embody any measures to extend the earnings help funds for the unemployed (or any social help funds for that matter).

It’s as if the Authorities has simply erased the plight of the jobless that it’s intentionally rising from the general public debate.

I discover that an appalling prospect.

‘Pink ink’ hysteria

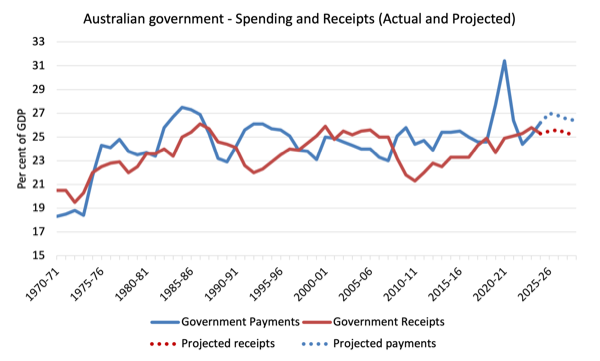

Right here is the fiscal place since 2000-01 with the pink bars indicating the forecast values.

Over the forecast interval there’s a slight contraction deliberate, which is why the unemployment charge is forecast to rise.

Final evening’s assertion indicated that the federal authorities could be in fiscal deficit eventually out to 2028-29, which has prompted the ‘pink ink’ hysteria brigade to prophesise all types of impending disasters.

What number of commentators are you able to rely that use phrases similar to ‘eye watering deficits’ or comparable.

Pathetic.

Since 1970-71, the fiscal deficit has averaged 0.9 per cent of GDP.

By 2028-29, it’s forecast to be 1 per cent of GDP.

If commentators would simply acquire some historic data, they is likely to be much less inclined to those excessive hysterics.

As I famous above, the fiscal deficit is too low – not extreme and there are numerous methods to exhibit that (see under).

The next graph exhibits the motion in these aggregates as a % of GDP since 1970-71.

The dotted segments are the fiscal assertion projections.

You possibly can see that whereas funds are projected to fall from 27 per cent of GDP in 2025-26 to 26.4 per cent in 2028-29, receipts are projected to stay comparatively steady and document 25.3 per cent of GDP in 2028-29.

Therefore the projected shrinking fiscal deficit by 2028-29.

Each spending and receipts are barely above their historic common at current.

However there’s nothing wild happening right here.

The fiscal help throughout the pandemic was substantial however now the aggregates are returning to ‘base’.

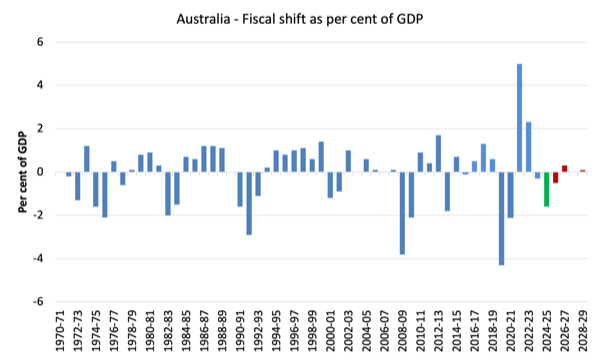

The fiscal shift from one yr to a different is the change within the fiscal steadiness as a proportion of GDP modifications.

It gives an concept of how expansionary or contractionary the present fiscal place relative to the earlier monetary yr.

It’s the results of two elements – the fiscal steadiness itself (in $As) and the worth of nominal GDP (in $As).

The next graph exhibits the current historical past (from 1970-71) of fiscal shifts as much as the tip of the projection interval (2026-27).

A constructive worth signifies a contractionary shift (even when the fiscal place remains to be in deficit) and vice versa.

I’ve colored the present fiscal yr (2024-25) inexperienced and the remaining pink columns are the ahead estimates for subsequent yr (2025-26) and people past.

The contractionary in 2021-22 was massive (a 5 per cent of GDP shift) because the Authorities deserted the pandemic help.

Within the first two years of the present Authorities (elected Might 2022), the contraction continued, with the Authorities relentlessly pursuing surpluses taking an additional 2.3 per cent of GDP out of the financial system in 2022-23 permitting two fiscal surpluses to be recorded.

However the contraction has killed financial progress and with a nationwide election simply weeks away, the Authorities has been pressured to take an expansionary place this yr earlier than resuming its shift to contraction.

The RBA rate of interest hikes that began in Might 2022 mixed with the fiscal shift this diploma of fiscal contraction is the rationale that GDP progress is now projected to be at ranges the place the unemployment charge rises considerably.

The place is the expansion coming from?

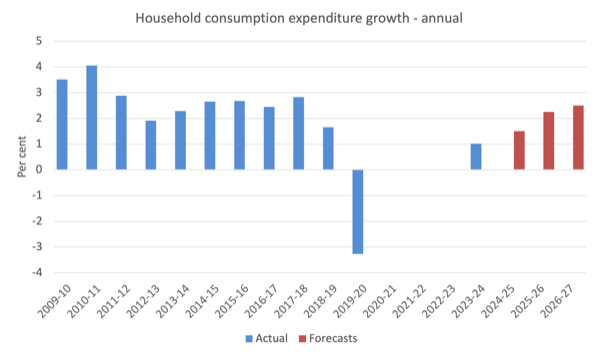

Because the Desk above exhibits, the Authorities is presenting an optimistic outlook for financial progress which seems to be pushed by a big ‘comeback’ in Family consumption expenditure.

The 2025-26 fiscal assertion forecasts that actual family consumption expenditure will develop by 0.75 per cent in 2024-25, then leap to 2.25 per cent within the subsequent two years.

The next graph exhibits the annual Family consumption expenditure progress from 2009-10 to 2026-27, with the pink bars capturing the Authorities’s projections (I deleted the pandemic outliers on each side of the zero axis).

I believe the ahead estimates of family consumption expenditure will likely be excessively optimistic.

Why?

As a result of the projected wages progress is overly optimistic given present tendencies and the delayed impression of the RBA rate of interest hikes and the fiscal contraction underway.

With the unemployment charge forecast to rise it’s exhausting to see wages progress sustaining the expansion predicted.

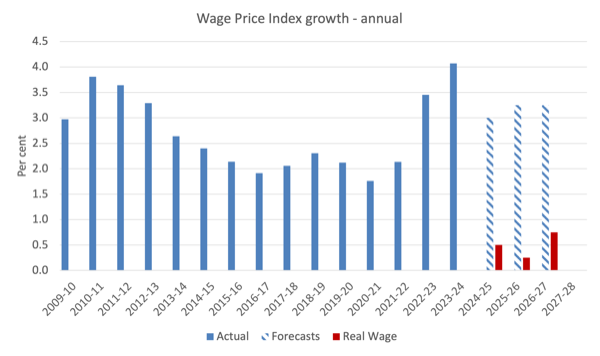

There will likely be some wages progress however nothing like that projected within the fiscal assertion (see the following graph).

Even with these optimistic nominal wage progress projections, actual wages progress is modest.

But when the wages progress is lower than predicted then there’s the likelihood that the true wage positive aspects is not going to materialise.

That leaves additional credit score progress to drive progress in consumption expenditure and with family debt at document ranges and rates of interest at elevated ranges, I can’t see that taking place.

Why the federal government technique is unsustainable

Trying again on the first Desk, we see that the expenditure drain from the exterior sector is predicted to extend relatively considerably over the forecast interval as the expected phrases of commerce decline considerably (Fiscal assertion – “sharper fall within the phrases of commerce).

The fiscal assertion additionally notes that:

Development in exports is anticipated to reasonable to 1 per cent in 2024–25, with companies exports progress slowing following the sharp rebound in schooling and tourism exports lately. Non-rural commodity exports are anticipated to stay subdued, reflecting ongoing weak situations within the Chinese language property sector.

Ally that with the data that the fiscal steadiness is forecast to say no.

Taken collectively it implies that non-public home demand should do the lifting and that implies rising indebtedness.

We all know that the monetary steadiness between spending and earnings for the non-public home sector (S – I) equals the sum of the federal government monetary steadiness (G – T) plus the present account steadiness (CAB).

The sectoral balances equation is:

(1) (S – I) = (G – T) + CAB

which is interpreted as that means that authorities sector deficits (G – T > 0) and present account surpluses (CAD > 0) generate nationwide earnings and internet monetary belongings for the non-public home sector to internet save total (S – I > 0).

Conversely, authorities surpluses (G – T < 0) and present account deficits (CAD < 0) scale back nationwide earnings and undermine the capability of the non-public home sector to build up monetary belongings.

Expression (1) may also be written as:

(2) [(S – I) – CAB] = (G – T)

the place the time period on the left-hand aspect [(S – I) – CAB] is the non-government sector monetary steadiness and is of equal and reverse signal to the federal government monetary steadiness.

That is the acquainted Trendy Financial Idea (MMT) assertion {that a} authorities sector deficit (surplus) is equal dollar-for-dollar to the non-government sector surplus (deficit).

The sectoral balances equation says that whole non-public financial savings (S) minus non-public funding (I) has to equal the general public deficit (spending, G minus taxes, T) plus internet exports (exports (X) minus imports (M)) plus internet earnings transfers.

All these relationships (equations) maintain as a matter of accounting.

The federal government is estimating that the adverse world elements will proceed to undermine Australia’s phrases of commerce.

They forecast a decline of two.5 per cent in 2024-25, then for an enormous contraction (-0.6 per cent) in 2025-6 and an additional fall of three per cent in 2025-26.

In different phrases, the commodity value increase which has pushed the exterior steadiness into surplus lately is forecast to finish and Australia will return to its normal place of a exterior deficit of round 3.5 to 4 per cent of GDP – a state that has been dominant because the Nineteen Seventies.

The present ‘commerce battle’ that the US authorities is waging with the remainder of the world will definitely add ripples into this image – on the draw back.

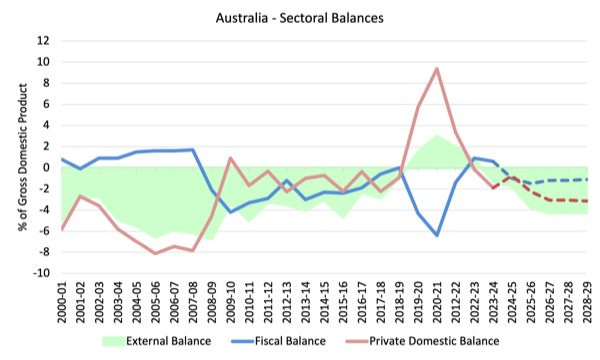

The next graph tells the story.

It exhibits the sectoral steadiness aggregates in Australia for the fiscal years 2000-01 to 2027-28, with the ahead years utilizing the Treasury projections revealed in ‘Funds Paper No.1’ in dotted type.

The projections start in 2024-25 (though the present yr’s outcomes are most likely going to be as forecast).

I’ve assumed that the exterior place in 2026-27 and past would be the identical because the Authorities’s estimate for that yr.

All of the aggregates are expressed when it comes to the steadiness as a % of GDP.

I’ve modelled the fiscal deficit as a adverse quantity despite the fact that it quantities to a constructive injection to the financial system.

You additionally get to see the mirror picture relationship between it and the non-public steadiness extra clearly this fashion.

So it turns into clear, that with the present account deficit (inexperienced space) projected to return rising deficits, which drain internet spending from the home financial system and with the fiscal steadiness transferring in the direction of zero over the identical interval, the non-public home steadiness (pink line) will head rapidly into increased deficits.

Increased non-public home deficits imply increased ranges of indebtedness.

The Family sector is already carrying document ranges of indebtedness which is why family consumption expenditure has been slowing down appreciably.

So replicate on that in relation to the earlier part on sources of progress.

You possibly can see that the pandemic help from Authorities clearly allowed the non-public home sector to rebuild its saving buffers and scale back the precarity of its steadiness sheet (given the large family debt).

Within the precedent days, previous to the GFC, the credit score binge within the non-public home sector was the one motive the federal government was in a position to document fiscal surpluses and nonetheless take pleasure in actual GDP progress.

However the family sector, particularly, accrued document ranges of (unsustainable) debt (that family saving ratio went adverse on this interval despite the fact that traditionally it has been someplace between 10 and 15 per cent of disposable earnings).

The fiscal stimulus in 2008-09 noticed the fiscal steadiness return to the place it must be – in deficit – given the nation’s exterior deficit place.

This not solely supported progress but in addition allowed the non-public home sector to start out the method of rebalancing its precarious debt place.

You possibly can see the pink line strikes into surplus or near it.

That course of was interrupted by the renewal of the fiscal surplus obsession in 2012-13.

The robust fiscal help throughout the pandemic overwhelmed all of the nonsensical deficit scaremongering and allowed the non-public home sector to extend its total saving (and pay down debt) which was a great factor.

However because the earlier authorities withdrew its stimulus and the present authorities continued to pursue a contractionary fiscal place (see above), the non-public home sector has just one possibility given the tendencies within the exterior sector if it needs to keep up consumption expenditure – resume the method of accumulating extra debt.

With a world recession threatening and with increased rates of interest the norm, the technique outlined in yesterday’s fiscal assertion is as soon as once more putting the financial system on an unsustainable path counting on family debt accumulation, which is a finite course of.

Conclusion

There are various different points to the present fiscal stance which I may talk about if I had extra time.

Generally, I’m unimpressed.

That’s sufficient for at this time!

(c) Copyright 2025 William Mitchell. All Rights Reserved.