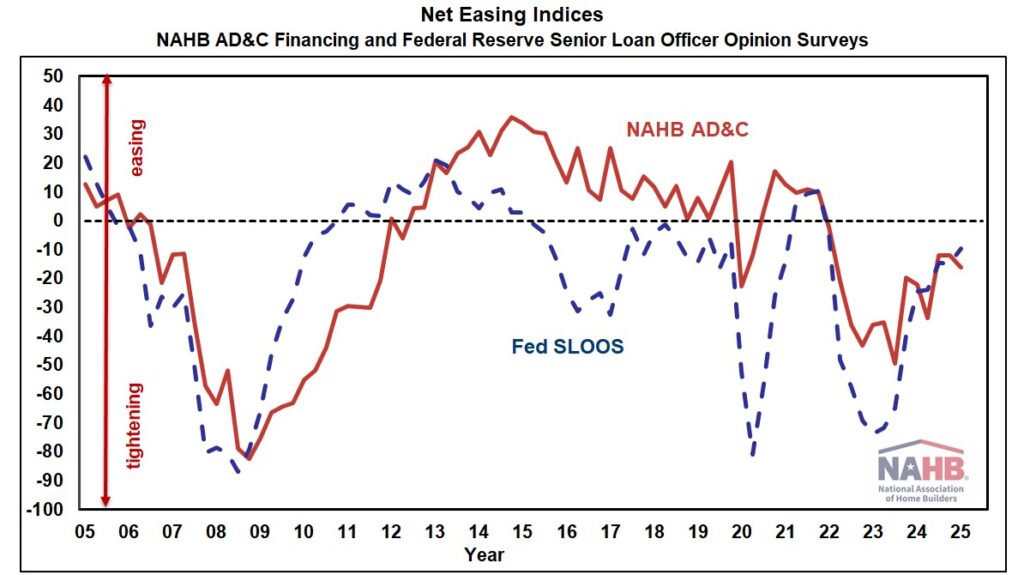

Debtors and lenders agreed that credit score for residential Land Acquisition, Growth & Building (AD&C) tightened additional within the fourth quarter of 2024, based on NAHB’s survey on AD&C Financing and the Federal Reserve’s survey of senior mortgage officers. The web easing index derived from the NAHB survey posted a studying of -16.3, whereas the same index derived from the Fed survey posted a studying of -9.5 (the adverse numbers indicating that credit score tightened for the reason that earlier quarter). Though the extra internet tightening within the fourth quarter was modest (as indicated by adverse numbers a lot nearer to 0 than -100), this marks the twelfth consecutive quarter throughout which each surveys reported internet tightening of credit score for AD&C.

In keeping with the NAHB survey, the commonest methods by which lenders tightened within the fourth quarter had been by reducing the loan-to-value or loan-to-cost ratio (reported by 72% of builders and builders) and lowering the quantity they’re keen to lend (61%). Further info from the Fed’s survey of lenders—together with measures of demand and internet easing for residential mortgages—is mentioned in an earlier submit.

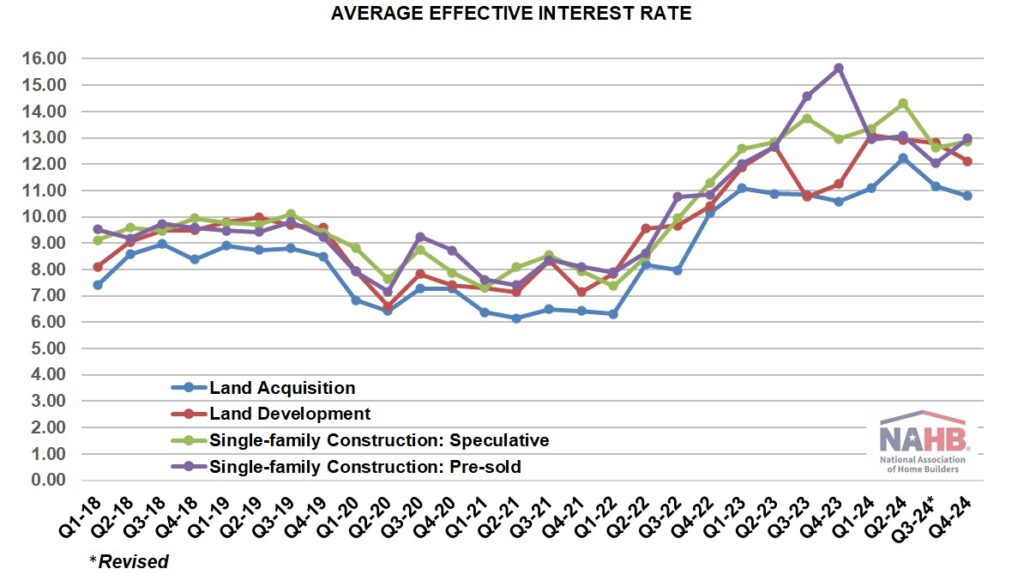

For the second consecutive quarter, the contract rate of interest declined on all 4 classes of loans tracked within the NAHB AD&C survey. Within the fourth quarter of 2024, the common contract rate of interest declined from 8.50% in 2024 Q3 to eight.48% on loans for land acquisition, from 8.83% to eight.28% on loans for land improvement, from 8.54% to eight.34% on loans for speculative single-family building, and from 8.11% to 7.75% on loans for pre-sold single-family building.

Along with the contract price, preliminary factors charged on the loans may be an necessary element of the general value of credit score, particularly for loans paid off as shortly as typical single-family building loans. Within the fourth quarter, tendencies on preliminary factors had been blended. The common factors declined on loans for land acquisition, from 0.77% in 2024 Q3 to 0.55%. Nevertheless, common factors elevated quarter-over-quarter on loans for land improvement (from 0.68% to 0.75%), pre-sold single-family building (from 0.26% to 0.67%) and speculative single-family building (from 0.49% to 0.64%).

Not surprisingly, the conflicting tendencies described above resulted in blended outcomes for the general value of AD&C credit score, as indicated by the common efficient rate of interest (which takes each the contract price and preliminary factors under consideration). Within the fourth quarter of 2024, the common efficient price declined on loans for land acquisition from 11.17% in 2024 Q3 to 10.79%, and on loans on land improvement from 12.82% to 12.12%. In the meantime, the common efficient price elevated on loans for speculative single-family building from 12.61% to 12.86%, and on loans for pre-sold single-family building from 12.03% to 12.98%. Even after these disparate adjustments between 2024 Q3 and 2024 This autumn, the common efficient rates of interest on all 4 classes of AD&C loans had been no less than barely decrease in 2024 This autumn than they had been in 2024 Q2.

Extra element on credit score circumstances for residential builders and builders is on the market on NAHB’s AD&C Financing Survey net web page.

Uncover extra from Eye On Housing

Subscribe to get the most recent posts despatched to your e mail.