These days, mortgage charges have been form of caught in a holding sample, although drifting decrease on the similar time.

Finally look, the 30-year fastened was priced at round 6.25%, which is fairly good within the grand scheme of issues. Undoubtedly decrease than the historic common of seven.75%.

Given charges had been nearer to 7% for many of the previous 52 weeks, it’s a good spot to be in.

They’re additionally mainly hovering simply above the bottom ranges seen over the previous three years, one other optimistic takeaway.

The query is how do they get their huge break and eventually duck beneath 6% once more?

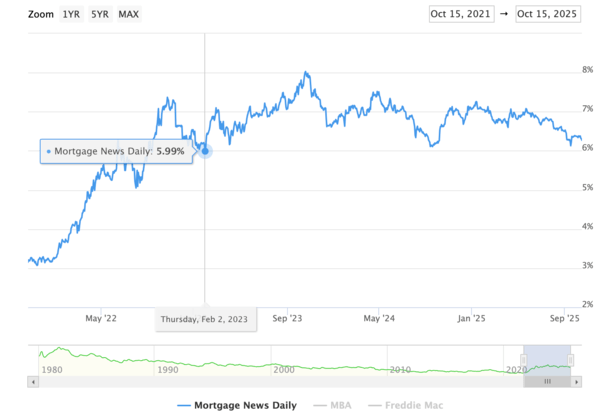

Mortgage Charges Are Near Breaking Beneath 6% for the First Time in Almost Three Years

Mortgage charges haven’t been sub-6% since February 2nd, 2023, at the least in response to Mortgage Information Every day.

And Freddie Mac hasn’t recorded a sub-6% studying for the 30-year fastened for the reason that week ending September eighth, 2022!

That’s a very long time. Almost three years now. In fact, they’ve been near these ranges at occasions since then.

And for the time being, they’re not far off in any respect. In actuality, householders are receiving mortgages that begin with 5 already.

But when we’re going to make use of a mortgage charge index just like the highly-cited MND, or Freddie Mac’s Main Mortgage Market Survey, we’re nonetheless above 6%.

So how will we get beneath that key psychological stage after almost 36 months? Properly, one of the best route is probably going continued financial weak spot and decrease inflation.

The issue proper now’s a scarcity of financial knowledge as a result of ongoing authorities shutdown, which is now on day 16.

Even with out it although, there are personal knowledge experiences and even other ways of amassing knowledge or gauging sentiment (OpenTable anybody?).

Neglect all that although. We’re almost at sub-6% ranges because it stands, so we don’t want numerous information to go a bit of decrease.

And as I’ve mentioned earlier than, mortgage charges are inclined to fall throughout authorities shutdowns anyway.

The place’s the Flight to Security?

Simply check out 10-year bond yields, that are the bellwether for 30-year fastened mortgage charges.

The ten-year yield is at the moment at 4.02%, doing a bit of standoff simply above the 3s. It has briefly dipped beneath 4% at occasions previously week, however hasn’t held there.

It continues to remain simply above 4% because it’s a degree of resistance. Simply because it appears 6% is a degree of resistance for shopper mortgage charges.

Right here’s the factor although. We’re knocking on the door to a sub-4% 10-year bond yield with out contemporary financial knowledge.

And we’re additionally doing so at a time when the inventory market is at/close to all-time highs!

Typically, shares and bonds have an inverse relationship, in that if one goes up, the opposite goes down and vice versa.

So if shares are crimson scorching, which they appear to be for the time being, it means bonds must be ice chilly. And if bonds are ice chilly, their related yield (or rate of interest) must be fairly excessive to draw traders.

Does that imply if and when shares take a breather, we’ll see a flight to security in bonds, which can lastly elevate bond costs and decrease their yields?

It definitely is smart, and given we’re already hovering simply above 4%, you possibly can envision a state of affairs the place we lastly bust via into the 3s.

Replace: As I used to be scripting this submit, the 10-year yield pushed beneath 4% on regional banking fears. The final time banks failed in early 2023, the 30-year fastened fell from round 7% to six% within the span of a couple of month.

Bond Yields May Push to the Low Finish of Their Vary

Again in Might, JPMorgan Asset Administration fastened revenue portfolio supervisor Kelsey Berro famous that the 10-year bond yield was buying and selling in a variety from 3.75% to 4.50%.

And with the Fed in a impartial if not arguably easing place, likelihood is we must be transferring to the bottom finish of the vary.

Assuming that occurs, and we get down to three.75%, mortgage charges ought to comply with, as they traditionally do.

If we at the moment have a 30-year fastened at 6.25%, you may see a path down to five.99% and even decrease.

It may even occur within the remaining three months of the 12 months, as there’s nonetheless loads of 12 months left in 2025.

You actually solely want a flight to security in bonds and a inventory market pullback, which many appear to consider is lengthy overdue.

We’ve acquired some sky-high valuations for the time being, an abundance of meme shares, together with mortgage and actual estate-related names, and normal euphoria taking place out there proper now.

So it wouldn’t be unrealistic to see a giant transfer from shares to bonds sooner or later over the subsequent few months.

As famous, we’re already virtually there anyway. Nearly 25 foundation factors and mortgage charges may very well be again to ranges final seen in 2022.

Learn on: The way to observe mortgage charges.

(photograph: Courtney)

Earlier than creating this web site, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and current) house patrons higher navigate the house mortgage course of. Comply with me on X for decent takes.