Think about waking up day-after-day realizing precisely how your cash is paving the way in which towards the long run you need. With YNAB targets, you possibly can pinpoint how a lot you want every month for all of the issues that matter to you—out of your childcare bills to your dream trip.

Browse common class setups and targets within the YNAB Templates Gallery!

Targets are on the coronary heart of many profitable YNAB spending plans. By setting predetermined quantities for every class, you not solely observe your progress towards monetary targets but in addition acquire a transparent view of your month-to-month monetary wants. YNAB simplifies this journey by turning your targets into actionable month-to-month targets, guaranteeing each greenback is aligned together with your priorities.

When you begin utilizing targets, it’s arduous to YNAB with out them!

And with the newest replace to targets in Might 2024, they’re simpler to make use of than ever earlier than. Being the savvy YNABer you might be, you’ll possible don’t have any hassle setting targets primarily based on the useful course of proper there in your cell or internet app. Simply in case, let’s dive into the straightforward four-step course of to arrange a goal in your YNAB spending plan.

Step 1: Select a cadence

Payments, bills, and financial savings targets are available all sizes and shapes. That is why YNAB flexes with you, adapting to the distinctive tempo of your life. Targets help you arrange weekly, month-to-month, or yearly cadences. For every part else, there’s the customized cadence choice, which we’ll go over in one other part. Let’s go over these commonest choices and the sorts of bills you’ll use them for.

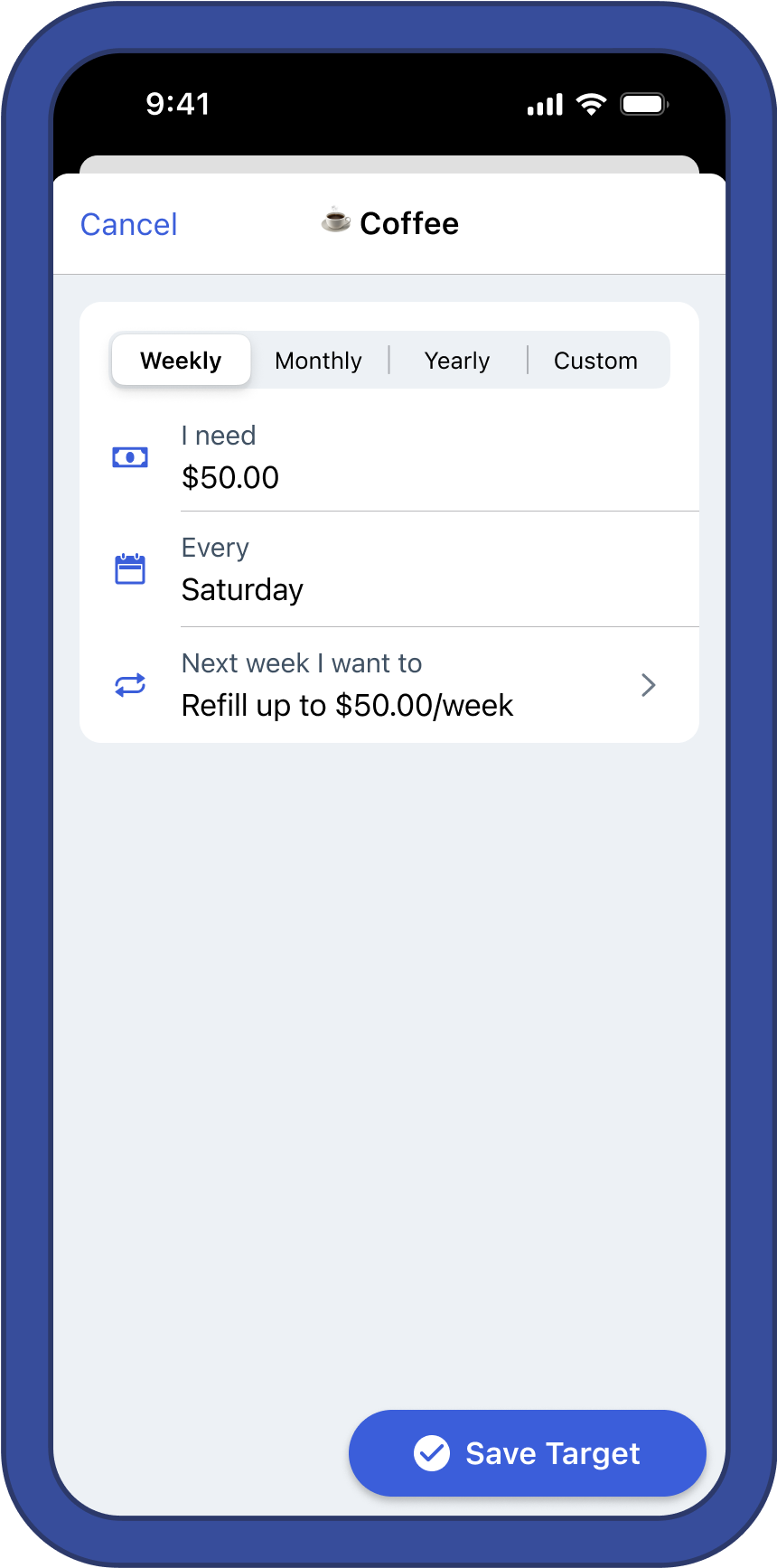

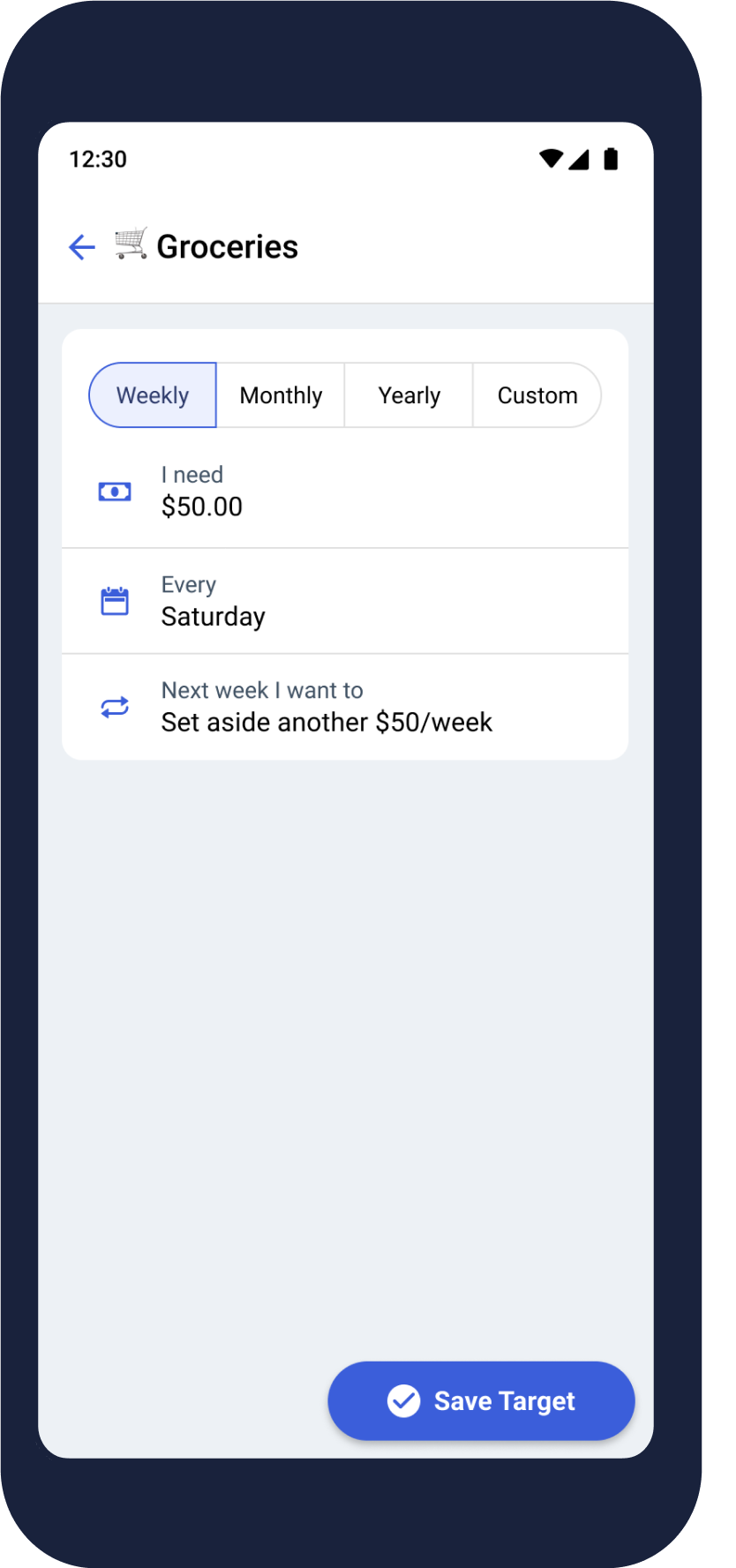

Weekly

Weekly targets are designed for any payments or bills that you just sometimes spend cash on as soon as per week. It’s excellent for that once-a-week childcare invoice, your routine journey to the grocery retailer, or your weekly date evening.

What’s good about weekly targets is YNAB will immediate you to assign a distinct quantity primarily based on the size of the month. So should you pay for childcare each Friday, YNAB will remind you when these pesky five-Friday months come alongside so that you at all times have sufficient.

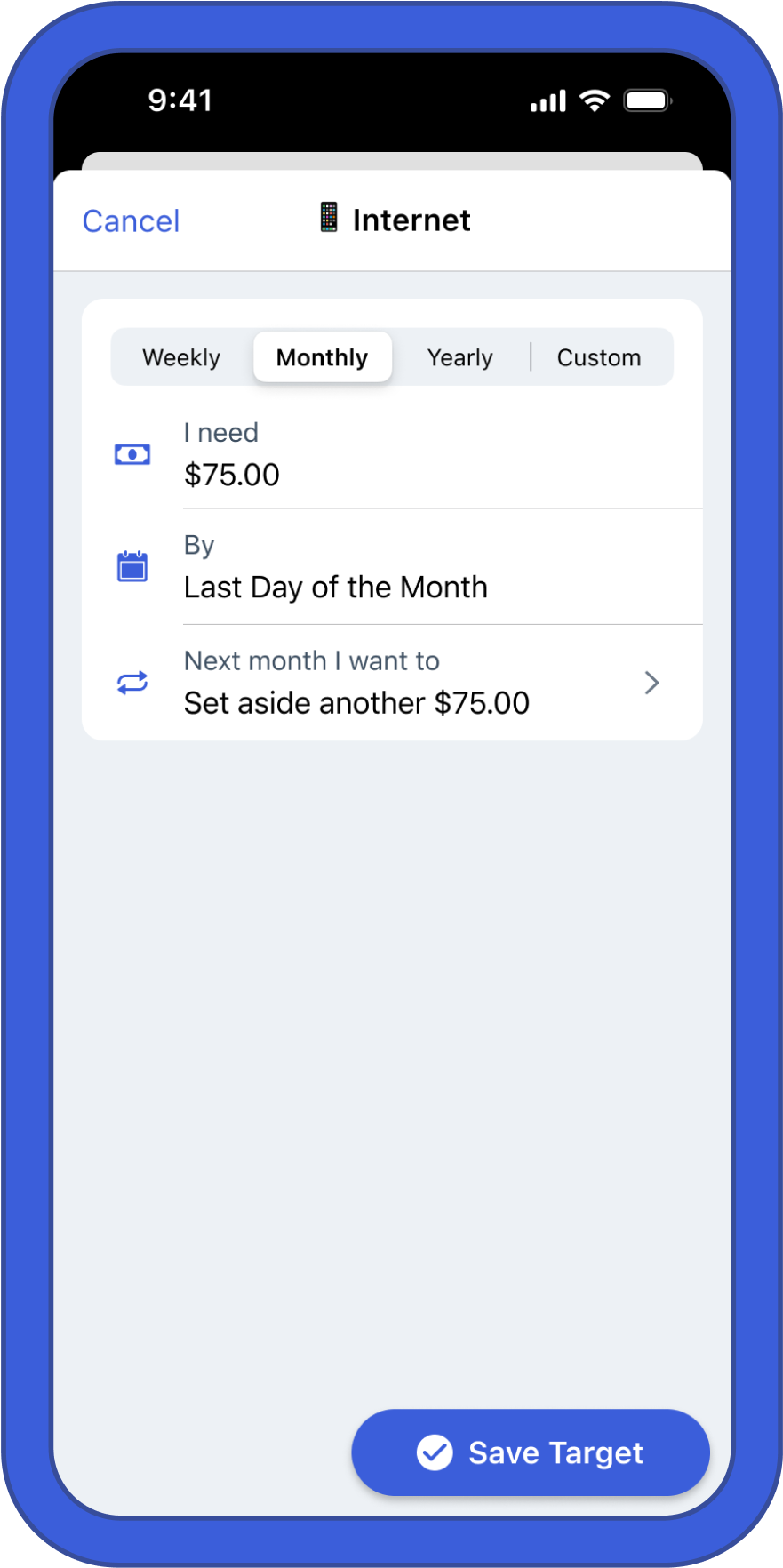

Month-to-month

Month-to-month targets are more likely to be the most typical in your plan. If you wish to put aside a certain quantity each month, that is the goal cadence for you. It really works for classes that you just spend from solely as soon as a month (like lease or your month-to-month cellphone invoice), but in addition for classes with variable spending patterns (like your private enjoyable cash).

You may even use it for unpredictable non-monthly bills that you just wish to set cash apart for each month, like automotive repairs. Use this everytime you wish to save or spend a certain quantity in a class each month.

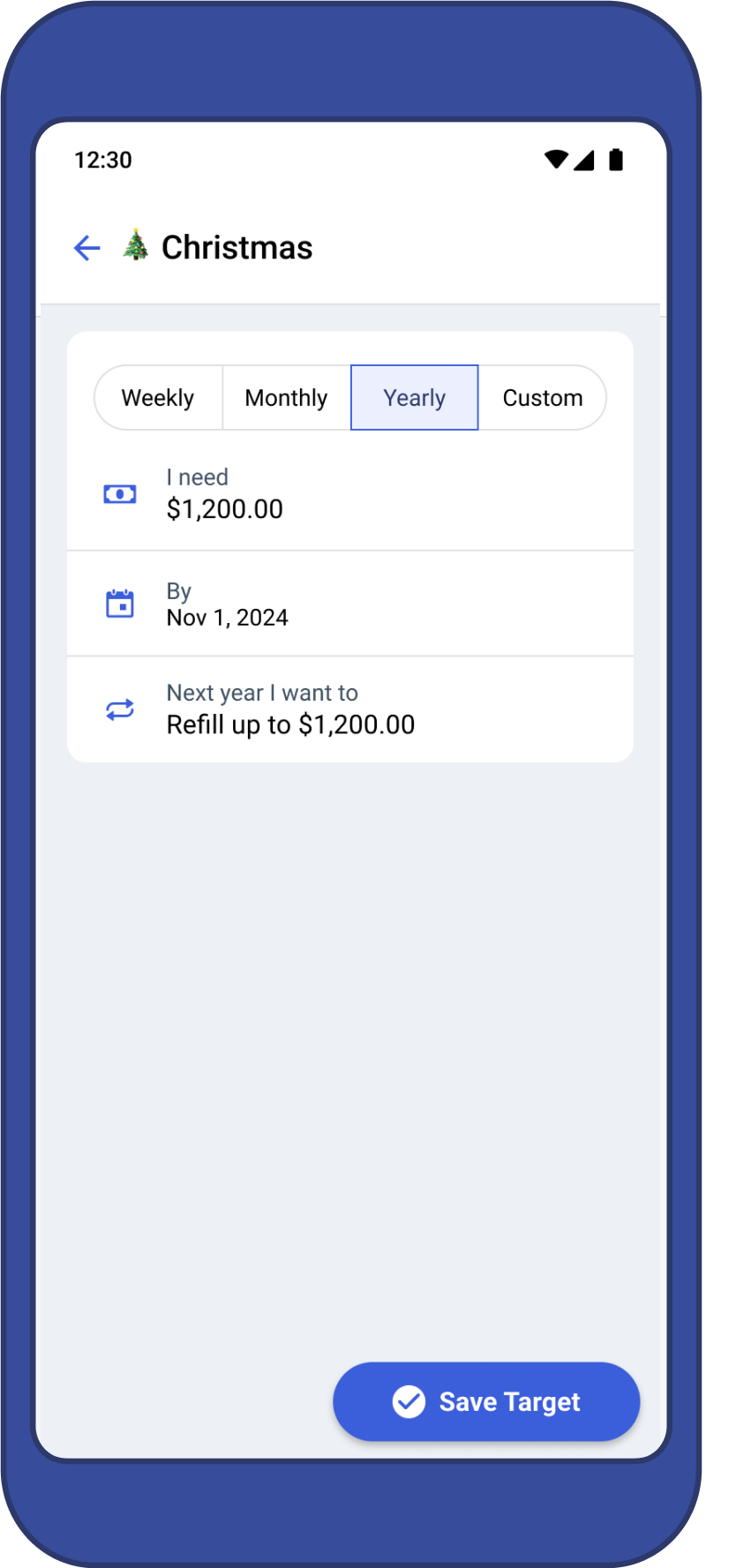

Yearly

Yearly targets are for all of your predictable yearly payments and bills. Suppose Amazon Prime cost, your property tax invoice, even your yearly YNAB subscription! When you’ve got a invoice that you just pay yearly like clockwork, the yearly goal will immediate you to save lots of sufficient each month to be prepared for it. No extra scrambling to cowl these massive yearly payments!

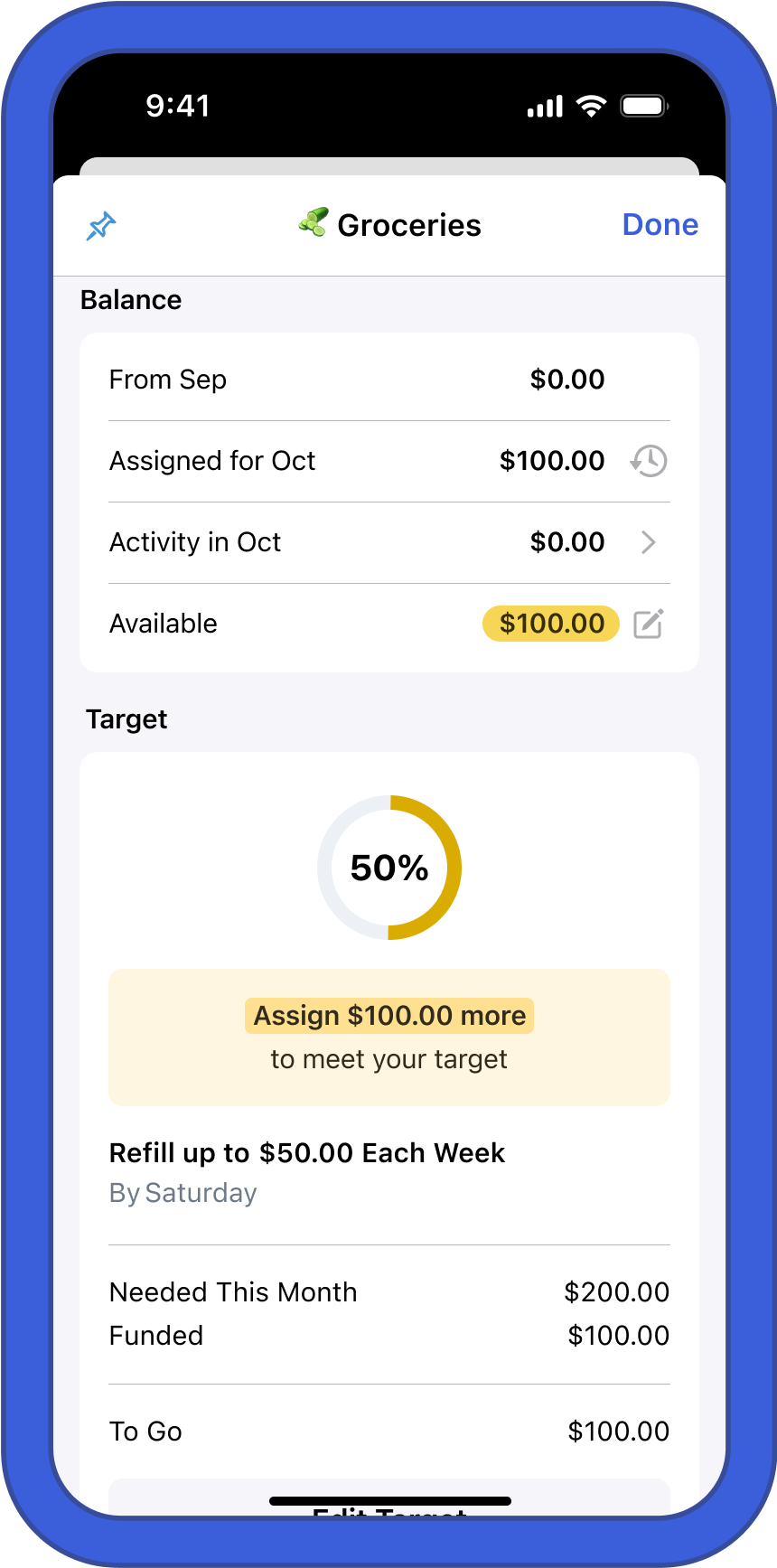

Step 2: Select an quantity

Below the goal cadence choices, you’ll see a number of extra fields to explain your bills in additional element. First you’ll see the phrase “I would like…” with a field so that you can enter in a quantity.

Naturally, each goal wants an quantity. How a lot cash do you want inside the time-frame of the cadence you selected in step 1? Write it down then cease worrying concerning the math. YNAB will take it from there!

Step 3: Select a due date

Subsequent, select a date that you just want the cash by. This area will look completely different relying on the cadence you selected in step 1.

For weekly targets, you’ll see the phrase “Each” and a drop down field with the times of the week. What day of the week do you sometimes spend cash in that class? In case you wish to go grocery purchasing on Mondays, select that day, and YNAB offers you a month-to-month goal quantity that modifications relying on what number of Mondays there are within the month.

For month-to-month targets, you’ll see the phrase “By” and a drop down field with the times of the month. When you’ve got a invoice that you just at all times pay on a sure day of the month, select that date. If it’s a financial savings objective or a extra variable expense, select “Final day of the month.” That is useful for notation functions.

With progress bars on, you’ll see the date that the invoice is due listed proper subsequent to the class title. However the date you select on month-to-month targets additionally impacts how the Underfunded Auto-Assign button auto-prioritizes your classes.

For yearly targets, you’ll additionally see the phrase “By” and a date picker the place you possibly can select the 12 months, month, and date of your yearly expense. This date will have an effect on how a lot cash YNAB prompts you to save lots of for yearly bills each month.

Step 4: Select a conduct

The final step is to inform YNAB the way you need the goal to behave as soon as the month rolls over or (within the case of yearly targets) the brand new yearly cadence begins. For weekly, month-to-month, and yearly targets, you’ll have two choices:

First, you possibly can put aside one other full goal quantity when it is time to fund the goal once more. That is the best and commonest choice. For weekly and month-to-month targets, you’ll proceed funding the identical quantity no matter how a lot cash rolled over from the earlier month or 12 months. Use this for normal payments, subscriptions, or for while you wish to save up cash in your class over time.

Second, you possibly can refill as much as the complete goal quantity when it is time to fund the goal once more. That is generally referred to as the “top-up” choice. This may set the goal to have your goal quantity available every month or 12 months. Something you don’t spend shall be utilized to subsequent month’s or 12 months’s goal.

Use this for classes the place you wish to spend a certain quantity each month or 12 months however don’t wish to lower your expenses over time. Gasoline, enjoyable cash, or eating out are widespread examples.

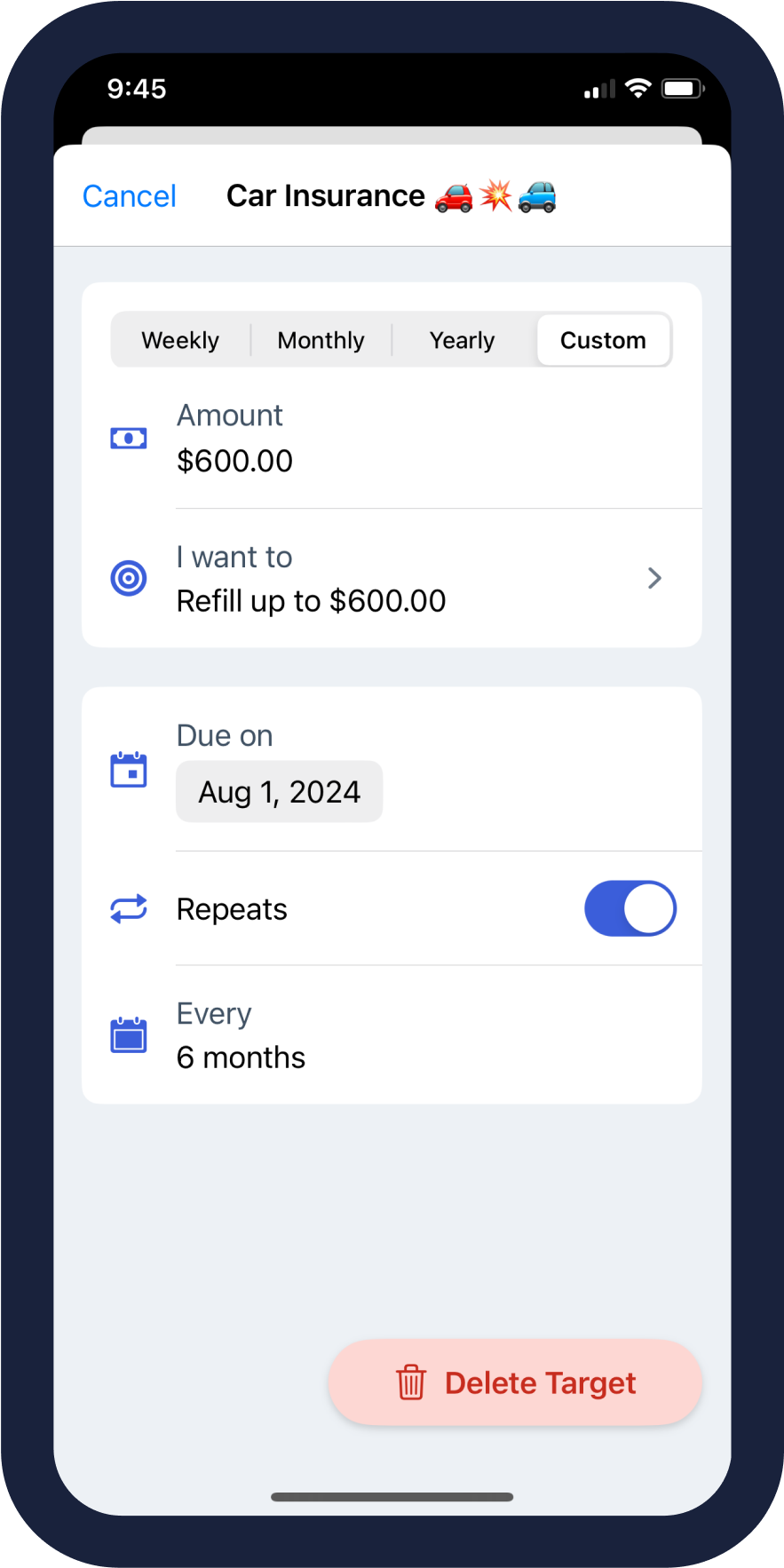

Customized targets—extra choices

In case you’re a extra seasoned YNABer, a real optimizer, otherwise you simply wish to have extra goal choices, the Customized cadence is for you! You’ll nonetheless set an quantity like the opposite choices, however the cadence is extra versatile. Select an applicable due date, then if the expense repeats, toggle on the “repeat” choice and select a customized cadence. You may set it to repeat each 1-11 months or each 1-2 years.

Some classes don’t want a repeating goal, as a result of they’re a one-off financial savings objective like a house down cost or a brand new Onewheel (I nonetheless haven’t damaged my collarbone, knock on wooden). For these sorts of bills, you’ll have a particular conduct that’s solely accessible for customized targets.

The “Have a Stability of…” conduct will set the goal to ensure you have a sure stability within the class by a sure date. In case you spend from this class alongside the way in which, YNAB will immediate you to assign extra in future months to play catch up.

You can too select the “Have a Stability of…” conduct on customized targets with out setting a date. YNAB received’t immediate you to put aside a certain quantity each month, however it is going to observe your progress towards your financial savings objective.

Bank card and debt cost targets

YNAB additionally has targets on classes which might be specifically paired to an account. Particularly, there are two choices for targets on bank card cost classes and Debt Fee Targets for classes paired with a mortgage account.

Bank card payoff targets

Credit score Card Fee targets are particularly for the bank card cost class that YNAB robotically creates while you add a bank card account. They’re designed that can assist you repay debt in your card from earlier months. There are two choices:

The Pay Off Stability by Date goal helps you to select a date you wish to have the cardboard paid off by. YNAB will calculate how a lot you have to put aside within the cost class primarily based on the date and your bank card stability.

The Pay Particular Quantity Month-to-month goal helps you to merely enter an quantity that you just wish to put aside each month to repay previous debt on the cardboard. YNAB will at all times immediate you to put aside that quantity it doesn’t matter what.

Debt cost goal

At face worth, the Debt Fee goal works precisely like a month-to-month goal. You set the month-to-month quantity and the date and YNAB will remind you to assign that quantity each month.

Debt cost targets robotically use the “put aside one other full goal quantity” conduct, which implies you’ll be prompted to put aside the complete goal quantity no matter how a lot cash rolled over from the earlier month.

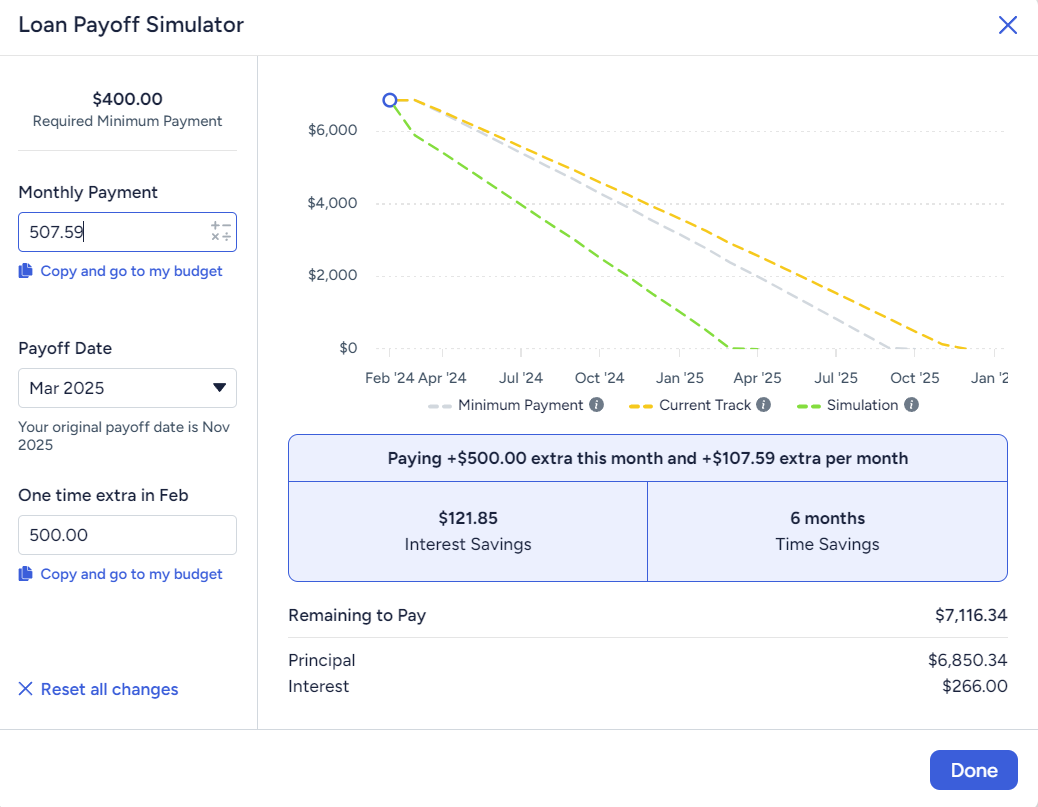

However the superior factor about Month-to-month Debt Fee targets is they’re specifically paired to a mortgage account, which incorporates additional knowledge visualization options and the Payoff Simulator, a sandbox that can allow you to dream a little bit with out altering something in your plan. If I make a one-time additional mortgage cost, how a lot curiosity will I save over 15 years? If I pay $100 additional each month on my automotive mortgage, how a lot quicker will I be capable to pay it off? The Payoff Simulator can reply these questions!

A simplified model of the Payoff Simulator can also be accessible within the finances display screen proper the place you set your goal.

In an effort to use a debt cost goal, you’ll first must arrange a mortgage account to pair with the class. In case you’d relatively not use a debt cost goal, you need to use a month-to-month goal as a substitute. However even should you’re not able to pay additional in your loans, it’s a good suggestion to go forward and use this goal in your debt cost classes so you possibly can simply unlock these instruments sooner or later.

Snooze a goal

We use targets to remind us how a lot we want in a class in a typical month. However not all months are typical. That’s what the Snooze a Goal function is for! If, for any motive, you don’t wish to totally fund a goal this month, you possibly can snooze it to take away the yellow underfunded alert till a brand new month begins. This lets you pause a goal with out eradicating it utterly.

We see individuals use this mostly in the midst of the month. In case you transfer cash out of a class to cowl overspending or fund a better precedence, the class’s accessible quantity will flip yellow to warn you that it’s underfunded. Even should you totally funded the goal in the beginning of the month, you’ll nonetheless get that warning while you make a change, so the Snooze function is ideal when that occurs.

Different instances, you simply can’t totally fund a goal this month, both as a result of your earnings was decrease than anticipated or as a result of a better precedence took desire. Snooze that focus on so that you don’t get the fixed underfunded alert, and also you’ll get a reminder to strive once more subsequent month. In case you constantly can’t fund a goal, it could be an indication that the class will not be a precedence or the quantity is unrealistic. In that case, take into account altering the goal extra completely.

With YNAB’s targets, you possibly can seize and slay each invoice and expense whereas making these monetary desires come true.

Cheers and comfortable YNABing!

Wish to keep within the know concerning the newest product updates and finest cash tales round? Join our YNAB newsletters—they’re brief, informative, and infrequently hilarious.