I used to be at an institutional investor convention again in 2011.

The inventory market had recovered considerably from the depths of the 2008 monetary disaster however loads of buyers had been nonetheless licking their wounds. Nobody was pounding the desk to purchase shares.

In reality, a well known hedge fund supervisor acquired up in entrance of the group and instructed everybody, “I’ve dangerous information for you…”

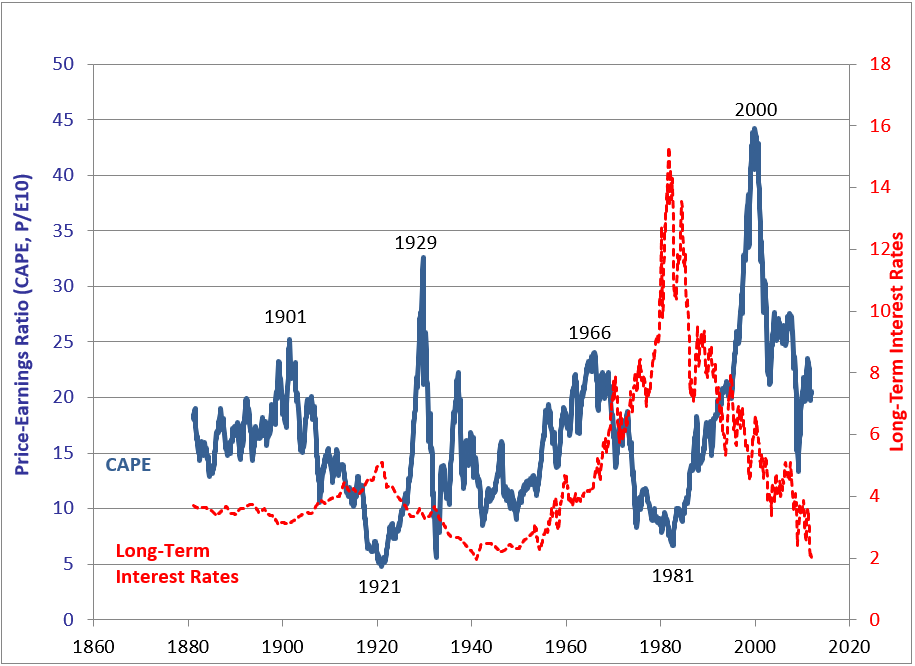

He then went by means of a collection of charts and historic information that confirmed how overvalued the inventory market was. The CAPE ratio was featured prominently and appeared like this on the time:

I don’t recall the precise figures, however he instructed the group we had been someplace within the 90-something percentile of worst valuations ever. The prospects for ahead returns from these ranges prior to now spelled bother. Mixed with low bond yields, buyers had been a decade of low returns.

That was his forecast anyway.

This well-known investor wasn’t alone in setting low expectations for future returns. The CIOs within the crowd largely agreed with him. Nobody anticipated a rip-roaring bull market to final for properly over a decade at that time.

Sam Ro has an awesome piece at TKer that appears at what went fallacious for the predictive energy of the CAPE ratio. Sam pulled some outdated quotes from CAPE creator, Robert Shiller:

“I’ve been very cautious about advising folks to drag out of the market although my CAPE ratio is at one of many highest ranges ever in historical past,” Shiller instructed Bloomberg in April 2015. “One thing humorous is occurring. Historical past is all the time arising with new puzzles.”

Shiller’s been warning folks in opposition to leaning on CAPE for some time.

“Issues can go for 200 years after which change,” he stated in a 2012 interview with Cash journal. “I even fear concerning the 10-year P/E — even that relationship may break down.”

That was little bit of humility on his half. The inventory market didn’t care concerning the earlier 10 years’ price of earnings when tech firms had been about to rewrite the foundations of revenue margins and market domination.

Simply because one thing labored prior to now doesn’t imply it can work sooner or later. Even when one thing does work fairly properly, it’s not assured to work each time. All the time and by no means are two phrases it is best to drop out of your vocabulary as an investor.

Peter Bernstein wrote about one thing that labored till it didn’t in his basic e book Towards the Gods:

In 1959, precisely thirty years after the Nice Crash, an occasion occurred that made completely no sense within the gentle of historical past. As much as the late Fifties, buyers had acquired a better revenue from proudly owning shares than from proudly owning bonds. Each time the yields acquired shut, the dividend yield on widespread shares moved again up over the bond yield. Inventory costs fell, so {that a} greenback invested in shares introduced extra revenue than it had introduced beforehand.

So it’s no marvel that buyers purchased shares solely after they yielded a better revenue than bonds. And no marvel that inventory costs fell each time the revenue from shares got here near the revenue from bonds.

Till 1959, that’s. At that time, inventory costs had been hovering and bond costs had been falling. This meant that the ratio of bond curiosity to bond costs was taking pictures up and the ratio of inventory dividends to inventory costs was declining. The outdated relationship between bonds and shares vanished, opening up a niche so large that in the end bonds had been yielding greater than shares by an excellent higher margin than when shares had yielded greater than bonds.

Have a look:

Bond yields by no means stayed above dividend yields till they did. Then it occurred for 5 many years.

Issues change.

The inverted yield curve was 8-for-8 at predicting previous recessions…till 2022 that’s. Brief-term bonds yields went above long-term bond yields however a recession didn’t comply with. The yield curve has since un-inverted and nonetheless no financial downturn.

That very same 12 months shares and bonds did one thing that had by no means occurred earlier than — they each crashed. Buyers assumed bonds all the time hedged a falling inventory market. Not when bonds trigger shares to fall.

Benoit Mandelbrot as soon as stated, “The pattern has vanished, killed by its personal discovery.”

The onerous half about all of that is that generally traits change eternally, they usually don’t return. Different instances, there are exceptions to the rule as a result of nothing works on a regular basis.

There’s a high quality line between self-discipline and an incapability to be versatile as an investor.

The answer right here is to keep away from going to extremes. There may be loads of grey space between 0% and 100% certainty.

Unfold your bets.

Robust opinions loosely held.

And go into any funding technique, historic market backtest or financial relationship with an open thoughts.

The market will humble you should you don’t strategy it with a way of humility.

Additional Studying:

The Half-Lifetime of Funding Methods