In case you’ve but to enter the housing market, however are considering of shopping for a house in 2025, there’s quite a bit it is advisable know. The 2025 housing market goes to be quite a bit completely different than in prior years!

As I as soon as identified, this isn’t your older sibling’s housing market. Not simply anybody can get a mortgage as of late. You really should qualify. However we’ll get to that in a minute.

Let’s begin by speaking about house costs, which surged lately and are lastly starting to maneuver sideways (and even decrease) after hitting all-time highs.

On the identical time, mortgage charges stay fairly elevated, having greater than doubled from their file lows over the course of 2023 and 2024, although they’re slated to fall (hopefully) because the yr goes on.

Taken collectively, house shopping for in 2025 ought to get a bit of simpler from an affordability standpoint, but it surely nonetheless isn’t low-cost and high quality stock stays scarce.

1. Put together for Extra Sticker Shock When Shopping for a Dwelling in 2025

In case you’re getting ready to purchase a house in 2025, anticipate to be shocked, and never in a great way.

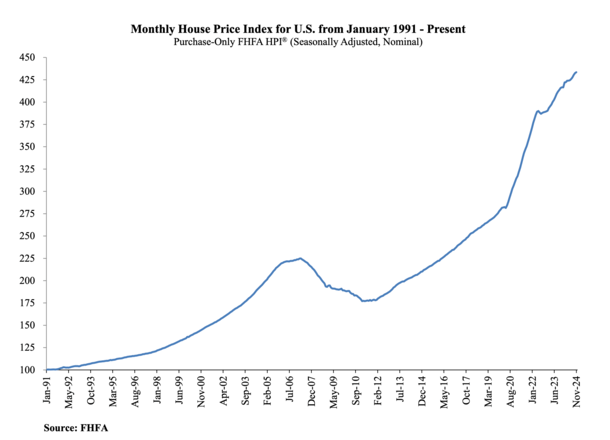

At this level within the cycle, house costs have eclipsed previous all-time highs in lots of elements of the nation, if not practically all locations.

And whereas appreciation is now on a downward trajectory, with marginal and even barely detrimental annual features anticipated, it stays constructive in most metros.

In different phrases, houses aren’t low-cost, nor do they appear to be happening sale this yr, regardless of these excessive mortgage charges.

Whereas some markets skilled a correction in 2022 and 2023, most are slated to rise in 2025 as they’ve in prior years, albeit at a slower tempo.

Wanting on the graph above from the FHFA, you may see that after a minor blip, costs marched greater and left their 2007 peak within the mud.

Many imagine mortgage charges and residential costs have an inverse relationship, however this merely isn’t supported by the information. Each can go up (or down) collectively.

Earlier than the pandemic-fueled loopy vendor’s market acquired underway, you can usually anticipate to pay beneath the Zestimate/Redfin Estimate. Actual property brokers even used to cover them!

Then it was all bidding wars and gives of $100,000 or extra above asking in scorching markets.

These days, there’s probability bids barely beneath asking will once more be accepted by extra lifelike sellers, however you should definitely have a look at the place costs have been only a couple years in the past.

Take a look at that property historical past part on Zillow or Redfin. What did they purchase it for and when? Are they promoting it for double the value after only a few years?

Is it really a screaming cut price? Or a slight low cost off what was as soon as an excellent inflated worth?

Sadly, stock stays extraordinarily tight and if charges come down there’ll possible be robust house purchaser demand, particularly for high quality properties in modern areas.

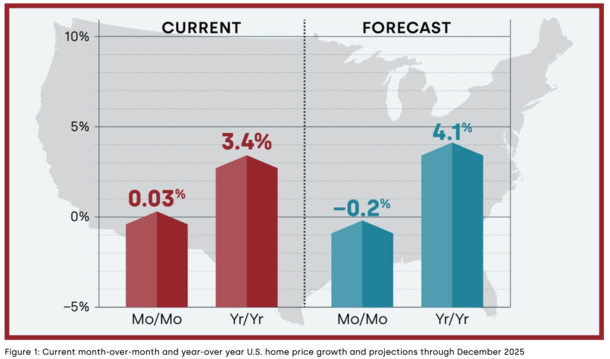

Dwelling Costs Nonetheless Anticipated to Rise 4.1% in 2025

The unhealthy information for renters is house costs are nonetheless projected to rise 4.1% on a year-over-year foundation from December 2024 to December 2025, per the CoreLogic HPI Forecast.

Briefly, anticipate to shell out a whole lot of dough if you need a house this yr, even when paying beneath asking (or getting a reduction vs. 2022 highs).

The mixture of a considerably greater mortgage fee and a still-high asking worth are sufficient to maintain sticker shock alive and effectively in 2025.

However in case you completely love the property, it is perhaps a small worth to pay to lastly put a irritating house search to relaxation.

The previous marry the home, date the speed adage might start to make extra sense if charges really do fall decrease in late 2025 and 2026.

2. Get Pre-Permitted for a Dwelling Mortgage Early On

Talking of that house nonetheless being out of your worth vary, it’s possible you’ll wish to get pre-approved with a financial institution, mortgage dealer, or mortgage lender ASAP.

First off, actual property brokers gained’t provide the time of day with out one, regardless that the market has cooled.

And secondly, in case you don’t know how a lot home you may afford, you’re mainly losing your time by perusing listings and going to open homes.

That is very true if mortgage charges creep again up as it is going to additional erode your buying energy. Both approach, take the time to know the place you stand. Don’t be complacent, even when others are.

It’s not onerous or all that point consuming to get a mortgage pre-approval, and it’ll offer you extra confidence and maybe make you extra severe about lastly making the transfer.

Learn extra about why you must search for a mortgage earlier than you seek for a house.

Tip: Search for an internet mortgage lender that permits you to generate a pre-approval on the fly in minutes (and know you don’t have to make use of them if and if you proceed with a house buy!).

3. Examine Your Credit score Scores and Put Away Your Credit score Playing cards

Whilst you’re at it, you must test your credit score scores (all 3 of them) and decide if something must be addressed. NOW!

As I all the time say, credit score scoring modifications can take time, so give your self loads of it. Don’t wait till the final minute to repair any errors or points.

And whilst you’re addressing something that wants extra consideration, do your self a favor and put the bank cards within the freezer (or some other place out of attain).

Likelihood is you’ve racked up some spending throughout the holidays, so it’s time to begin paying it off.

Numerous spending, even in case you pay it again straight away, can ding your scores, even when simply momentarily.

This has grow to be much more necessary as a result of Fannie Mae and Freddie Mac now need debtors to have a 780 FICO rating for the easiest pricing.

Excellent debt also can enhance your DTI ratio and restrict your buying energy in case you don’t pay it off. In the end, unhealthy timing can create massive complications within the mortgage world.

As well as, pumping the brakes on spending would possibly offer you a pleasant buffer for closing prices, down fee funds, transferring prices, and renovation bills when you do purchase.

Talking of property, cease messing with them and maintain them in a single account that may be simply verified when you apply for a house mortgage.

This implies no incoming or outgoing transfers aside from direct deposits out of your job. A cleaner financial institution assertion will make life quite a bit simpler for everybody, together with your underwriter!

4. High quality Housing Stock Will Be…Restricted

It’s the identical story in 2025 because it was in 2024, 2023, 2022, 2021, and heck, even way back to 2012.

There’s been a scarcity of stock for the reason that housing market bottomed as a result of houses have been by no means on the market en masse.

That is the actual cause behind the file house worth development seen lately. The low mortgage charges simply added gasoline to the fireplace.

Throughout the prior housing disaster, debtors acquired foreclosed on or deployed actual property brief gross sales to maneuver on, and banks made positive all that stock by no means flooded the market.

Others rode it out and at the moment are in unimaginable positions with tons of house fairness simply ripe for the tapping.

Right this moment, we’ve acquired tens of millions of would-be sellers with nowhere to go, because of the large worth will increase realized over the previous few years.

And the lock-in impact of low mortgage charges they don’t wish to go away behind.

In the end, it’s onerous to maneuver up or downsize, so a whole lot of people are staying put. Which means much less alternative for you in case you’re nonetheless a renter.

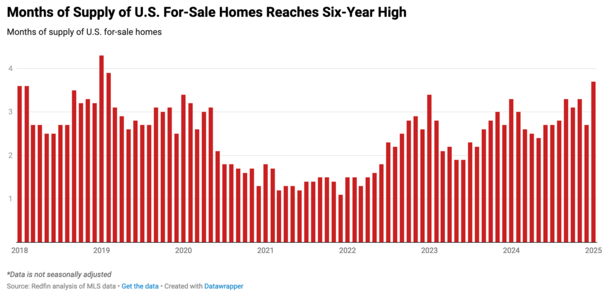

Whereas we’ll see an uptick in stock in 2025 because of a scarcity of affordability and vendor impatience, the housing provide remains to be extremely low traditionally.

On the finish of December, the Nationwide Affiliation of Realtors mentioned unsold stock was at a 3.3-month provide on the present gross sales tempo, down from 3.8 months in November however up barely from 3.1 months a yr in the past.

This stays beneath the 4-5 months of provide thought-about wholesome. So mortgage charges apart, we’ll proceed to have a provide/demand imbalance.

The caveat is new houses is perhaps in better provide because of elevated constructing, although they’re usually in less-central places the place uncooked land was extra available to house builders.

With falling mortgage charges and a number of People hitting the ripe first-time purchaser age of 34, anticipate competitors to accentuate because the yr goes on, even when not as unhealthy as latest years.

Once more, this helps the argument of being ready early so that you’re able to make a proposal at a second’s discover!

5. The Dwelling You Purchase Would possibly Be a Fixer Higher

You most likely don’t have the identical talent set as Joanna and Chip Gaines, however you would possibly nonetheless wind up with a fixer-upper because of these huge stock constraints. And that’s completely okay.

What I’ve realized from shopping for actual property is that you’ll sometimes by no means be content material with the upgrades earlier house owners or builders make, even when they have been tremendous costly and top quality. So why pay additional for it?

Particularly if the house comes adorned with grey flooring and different traits which can be quickly going out of favor.

There’s probability you’ll wish to make the house yours, with particular touches and modifications that distance your self from the earlier proprietor.

Don’t be afraid to go down that street, but additionally know the distinction between superficial blemishes and design challenges, and main issues.

Particularly this yr, be careful for cash pits that sellers are desperately seeking to unload as a result of they missed the highest of the market might now be panicking.

These properties that would by no means promote might hit the market once more, however you may not need that purchaser to be you.

With extra steadiness within the housing market, and fewer strain to waive contingencies, take the time to get a correct house inspection (or two) and go to the inspection your self!

Observe: The share of all-cash house purchases fell to 32.6% in 2024, a three-year low per Redfin, as the entire variety of all-cash transactions hit its lowest degree in a decade.

This implies traders are shopping for much less, which might spell alternative. Simply be cautious of their lowered urge for food signaling a market high.

6. You Might Nonetheless Must Combat for the Property

What’s much more annoying is that you’ll have to battle to get your arms on the few high quality properties which can be on the market, relying on the housing market in query.

I used to be talking with my endodontist (sure, endodontist) the opposite day and he introduced up level.

Having had bought a property a yr or so in the past, he talked about how at the moment’s house patrons are more and more determined.

So if and once they do come throughout one thing they even remotely like, they’re prepared to go above and past.

And which means even when 2025 is a cooler housing market, scaring off different would-be patrons within the course of.

If the property is fashionable, there’ll all the time be somebody prepared to outbid you for that house they only will need to have. That is another excuse why the fixer generally is a winner, the hidden gem if you’ll.

That being mentioned, it’s okay to pay full ask (and even the absolutely appraised worth), simply needless to say there are many different fish within the sea.

Nicely, maybe not loads proper now, however there’s all the time one other alternative across the nook.

Keep poised and don’t let your feelings get one of the best of you. Like the rest, it’s okay to stroll away. Belief your intestine.

7. Completely Negotiate with the Dwelling Vendor (and Actual Property Agent)

It appears clear that like prior years, 2025 is not going to be an outright vendor’s market.

Nevertheless, circumstances have cooled over the previous couple years, with 2024 displaying indicators of weak spot and 2025 shaping as much as be the second yr in a row the place we’ll see extra equilibrium between patrons and sellers.

For instance, Redfin reported that the everyday house offered for 1.8% lower than its ultimate asking worth in January, the biggest such low cost in practically two years.

And regardless of stock being low, months’ provide is the very best it has been since February 2019 (granted January isn’t an awesome gauge as a result of gross sales are sluggish throughout the begin of the yr).

Your Particular person Housing Market Might Fluctuate

However provide is unquestionably up, and that is very true in sure Solar Belt states equivalent to Florida and Texas.

Cape Coral, FL at the moment leads the nation in out there stock at 11.6 months of provide as of January, up from 8.6 months a yr in the past.

Miami isn’t far behind with 11.4 months of provide, up three months year-over-year, adopted by McAllen, TX at 10.5 months, up 2.5 months YoY.

On the opposite aspect of the coin, Rochester, NY had simply 1.1 months of provide in January, the least within the nation.

Buffalo, NY wasn’t significantly better at 1.2 months of provide, nor was Hartford, CT (1.4 months of provide), Grand Rapids, MI (1.5 months of provide), or Worcester, MA (1.6 months of provide).

The takeaway is to take a tough have a look at your native housing market and ignore the nationwide noise, which could not be related.

Lastly a Purchaser’s Market in 2025?

After all, Redfin is now proclaiming that we’re in a purchaser’s market, with Redfin Economics Analysis Lead Chen Zhao saying, “that is first time we will say that patrons have as a lot, if no more, energy than sellers” this decade.

So even in fashionable markets, you would possibly be capable to negotiate on worth, contingencies, repairs, and many others.

Whilst you’re at it, negotiate the fee your actual property agent expenses. Whereas it by no means hurts to ask, your probabilities of success could possibly be higher in 2025 because of ongoing fee lawsuits.

On the identical time, it’s nonetheless attainable you can get right into a bidding battle. If that occurs and also you win the factor, you should definitely examine the heck out of the home.

Inspections are key to figuring out what’s going to must be addressed as soon as the house modifications arms, and what the vendor might want to do to compensate you for these points.

Positive, the vendor might say it’s being offered as-is, however you may nonetheless say what about this, that, and that different factor?

In case you don’t get a high quality inspection (or two), you’ll have a troublesome time asking for credit for closing prices or perhaps a decrease buy worth. Take it very critically, the return on funding will be staggering.

Numerous native actual property markets have cooled considerably, so that you would possibly be capable to bid beneath asking AND nonetheless get cash for repairs.

You must also inquire about vendor concessions, and a attainable mortgage buydown to snag a decrease fee the primary 1-3 years on your own home mortgage.

Take a second to raised perceive your goal market by taking a look at not too long ago closed listings on web sites like Redfin and Zillow. Examine what they initially listed for and ultimately offered for.

In the event that they’re persistently promoting beneath record, you understand it’s going to be a comparatively simple purchase. If not, effectively, get your negotiating hat on.

In locations that have been beforehand scorching, like Austin, Boise, Las Vegas, and Phoenix, offers is perhaps simpler to come back by. Simply be careful for falling house costs after you purchase. Some metros could possibly be prone to cost declines.

8. All the time Do Your Mortgage Homework

Whilst you may need your arms full with an overzealous actual property agent, it’s necessary to not neglect your own home mortgage.

Mortgages are sometimes simply mailed in, with little consideration given to the place they’re originated, or what worth is paid.

Your actual property agent can have their most popular lender that you just “actually ought to think about using as a result of they’re one of the best,” however you don’t have to make use of them and even communicate to them.

I’ll sometimes say get a quote from them as a courtesy to maintain issues amicable, and to appease your agent, but additionally store round with different banks, credit score unions, lenders, and mortgage brokers.

On the identical time, take into consideration the way you wish to construction the mortgage, together with down fee, mortgage kind (FHA or typical), and mortgage program.

The 30-year fastened isn’t all the time a no brainer, although you would possibly be capable to get a free buydown from the lender (Inflation Buster) or vendor that makes it low-cost for a pair years (or the lifetime of the mortgage).

There are different mortgage applications that may make sense too, such because the 5/1 ARM, which frequently get swept underneath the rug. Make sure to make the selection your self.

Additionally maintain a really shut eye on charges and fee as mortgage lenders are charging a number of low cost factors as of late in an unsure mortgage fee surroundings.

Watch out paying mortgage low cost factors as charges are anticipated to go down this yr and subsequent. And you can go away cash on the desk in case you refinance earlier than recouping the upfront price.

9. Anticipate a Barely Higher Mortgage Fee Than Final Yr

In case you’ve achieved your homework and are in good monetary form, you must be capable to get your arms on an honest mortgage fee in 2025.

The truth is, mortgage rates of interest are traditionally “not unhealthy” in the intervening time, regardless of doubling over the previous couple years.

Positive, your fee might begin with ‘6’ as a substitute of ‘3’ however that’s life. And a mid-6% 30-year fastened remains to be a fairly whole lot, particularly in case you’re capable of get the property for 10-20% off its latest highs.

It must also be markedly higher than the 8% mortgage charges on provide in 2023.

The 2025 mortgage fee forecast appears principally favorable, so we may even see some reduction because the months go by, with charges presumably within the high-5% vary sooner or later.

When it comes to financing, it’s nonetheless an OK time to purchase a house. However when you issue within the sky-high costs, the argument to lease vs. purchase begins to sound intriguing in some markets.

Both approach, be additional prudent in the case of choosing a lender to make sure you get one of the best fee and the bottom charges, even when charges proceed to fall.

In the intervening time, there may be a whole lot of divergence in pricing among the many lenders nonetheless working, so store judiciously.

10. The Finest Time to Purchase Would possibly Be Later within the Yr

Earlier than you get too excited watching house costs cool and mortgage charges trickle again down, it would really be in your favor to sluggish play this one.

Per Zillow, one of the best time to purchase a house could also be in late summer season, together with the months of August and September.

Mainly, you’ve acquired the sluggish, chilly months at the beginning of the yr the place there isn’t a lot stock, adopted by the robust spring housing market the place everybody and their mom unexpectedly needs to purchase.

That is sometimes when asking costs peak throughout the yr and in addition when mortgage charges are highest.

Then you definitely get a lull and maybe a dip in house costs throughout summer season, which could possibly be a lovely entry level.

You would possibly even get fortunate and snag a giant worth lower with quite a bit much less competitors whereas different potential patrons are on trip.

The icing on the cake is that mortgage charges are anticipated to fall extra within the second half of the yr, so that would double your potential victory.

In my 2025 housing market predictions submit, I famous that house costs and charges might each fall later within the yr.

Regardless, get pre-approved NOW and arrange your alerts for brand spanking new listings ASAP and simply be able to pounce every time. Don’t try to time the market ever!

11. Are You Really Positive You Wish to Purchase a Dwelling?

Lastly, take a second to make sure you really wish to purchase a house versus persevering with to lease.

I always hear the previous “throwing away cash on lease” line and it by no means will get previous. Then I proceed to fantasize about renting with not a care on the earth.

Are you positive you’re throwing away cash on lease? Renting will be fairly superior.

You don’t pay property taxes, householders insurance coverage, HOA dues, PMI, or mortgage curiosity. And you may go away everytime you need. That appears like a candy deal too.

Oh, and if something goes mistaken, you may simply name your landlord or property administration firm. Simple peasy.

With a house, the issue is yours, and yours alone to cope with. Damaged water heater? You’re paying hundreds out of pocket, not the owner.

And with house costs so excessive, watch out to not grow to be home poor in trade for coming into the housing market. Ensure you’ve acquired reserves available if and when stuff goes mistaken.

It’s not onerous to overextend your self in at the moment’s housing market, so ensure you’ve acquired an emergency fund after paying all of your closing prices.

Watch Out for the Authorities Layoffs and a Attainable Recession in 2025

One ultimate factor to think about given the brand new presidential administration and its DOGE initiative is widespread authorities layoffs, which might spark a recession sooner or later in 2025…

Sure, we heard this in 2023 and 2024 as effectively and it didn’t materialize. At the moment, economists believed there was a 70% probability of a recession.

The percentages of a recession for 2024 fell to roughly 52%, per Statista, which amounted to a coin flip.

And so they’re even decrease this yr, although with the shakeup that has occurred in only one month, between tariffs and authorities layoffs, this likelihood might skyrocket.

This will influence your choice to purchase a house, with maybe the most important situation being attainable unemployment, particularly these working in federal authorities and/or positioned close to D.C. and Virginia.

There have been a whole lot of layoffs recently, and there are most likely much more within the pipeline, sadly.

These vulnerable to job loss clearly should be tremendous aware a few potential house buy. Ensure you’re in place to make that massive monetary step.

Throughout recessions, house costs don’t essentially go up or down, however gross sales quantity typicallys drop as house owners hunker down. Since they’re already hunkered down with their low charges, it might additional squeeze provide.

With regard to financing, mortgage charges are likely to fall throughout recessions, which could possibly be a silver lining.

In the end, you must all the time give a house buy a ton of thought, so for me not a lot has modified on this entrance.

It doesn’t essentially should be placed on maintain, but it surely would possibly require extra analysis given the elevated uncertainty with the financial system, demographic shifts (metropolis vs. suburban residing), and so forth.

Additionally, suppose earlier than you make a whole way of life change like transferring out of the town and into the nation, simply because it’s on-trend. You would possibly look again in a yr or two and say what was I considering?! Ever seen Humorous Farm?

Extra Dwelling Gross sales in 2025 as Costs Stage Off: However Be Ready to Maintain if You Purchase

I imagine the 2025 housing market shall be a bit of brighter in comparison with 2024, however nonetheless difficult for many.

This implies incrementally greater house gross sales and higher equilibrium for patrons and sellers with barely decrease mortgage charges. However nonetheless a dearth of high quality provide.

Fannie Mae is at the moment forecasting 4.15 million current house gross sales, up from 4.05 million in 2024. And new house gross sales are anticipated to rise from 689,000 to 738,000.

When it comes to costs, they’re slated to rise however not as a lot as 2024. This implies shopping for a house in 2025 will stay costly, although newly-built houses is perhaps considerably of a deal if house builders proceed to supply massive concessions.

In case you’re questioning if 2025 shall be yr to purchase a home, that’s one other query.

I anticipate costs to degree off this yr and doubtlessly stay flat for the foreseeable future. They might even go down on a nominal foundation. The appreciation get together has actually come to an finish.

So anticipating massive features anytime quickly after buy is perhaps a tad optimistic. In different phrases, be ready to maintain your own home for chunk of time.

In any other case promoting could possibly be a difficulty in case you don’t have sufficient fairness to cowl transaction prices.

However ideally, there would be the probability to refinance to a decrease fee to save lots of in your mortgage if charges go down as anticipated within the second half of 2025.

Learn extra: When to search for a home to purchase.

Earlier than creating this website, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and current) house patrons higher navigate the house mortgage course of. Observe me on X for warm takes.