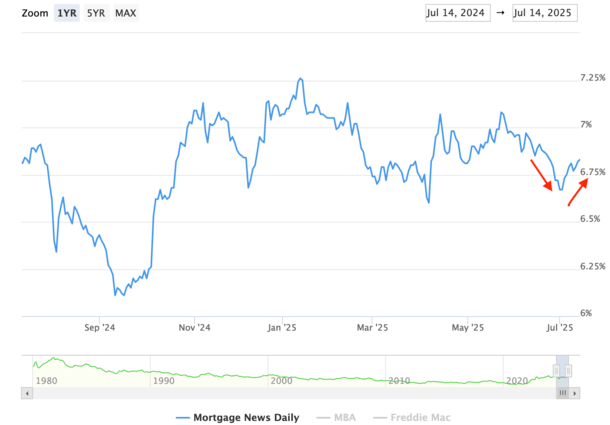

What a distinction a month makes. Mortgage charges had been near eight month lows about two weeks in the past.

Right now? They’re solely 17 foundation factors (0.17%) away from 7% once more, which explains the continued shift to a purchaser’s market.

It appears each time we make some strong progress, it’s one other step again to the place we began.

The newest drivers of upper mortgage charges have been resilient jobs information and one other spherical of tariff drama.

If this continues, it’s going to be troublesome to see any sustained enchancment any time quickly.

Resilient Jobs Information and Tariff Drama Pushes Mortgage Charges Again Towards 7%

The 30-year mounted started the month of July at a comparatively engaging 6.67%, earlier than marching again up towards 7%.

Eventually look, it stood at 6.83% after struggling one other sequence of setbacks, the primary being an unexpectedly sizzling jobs report.

That’s been the wrongdoer for some time now, as labor has but to actually break, and the Fed has famous it’s labor they’re taking a look at most intently.

There have been scattered studies on the upside and draw back, however we’ve but to see constantly dangerous labor information.

Till that occurs, it appears we’re sort of caught at larger ranges. Although earlier than the June jobs report beat (147k vs. 110k), mortgage charges had been starting to indicate some actual promise.

In truth, the 30-year mounted had fallen to six.67%, per Mortgage Information Each day, its lowest level of 2025 aside from a blip in early April associated to tariff drama.

Earlier than that, you needed to go all the best way again to October 2024 to see decrease mortgage charges.

And if you happen to recall September 2024, when mortgage charges slipped very shut to six%, it was a wholly completely different housing market.

One filled with promise and pleasure that the excessive mortgage charges might lastly be behind us. We additionally skilled a mini refi growth that had lenders feeling a bit extra optimistic.

Nevertheless, it was yet one more head pretend as sizzling jobs and now renewed tariff pressures push charges again up.

The newest being a 35% tariff on Canada, 30% on the EU and Mexico, and a tariff menace to Russia as nicely through “100% secondary tariffs concentrating on Russia’s remaining commerce companions if a peace cope with Ukraine” isn’t reached inside 50 days.

So if you happen to thought the tariff stuff was over, welp, it’s not. And who is aware of what’s subsequent.

Maybe I spoke too quickly after I mentioned the tariff stuff was within the rear-view mirror.

CPI Report Tomorrow Might Shed Gentle on Tariff Impression

Talking of the tariffs, tomorrow we get the ever-important CPI report, which would be the first time we get to see the influence of tariffs.

Although some have argued that “many firms stockpiled items upfront of the tariffs,” that means any worth will increase may not make their method into the info till that stock is offered off.

And with new tariffs being threatened as soon as once more, some starting August 1st, it continues to make it troublesome to find out who precisely is/pays for the tariffs.

Between the stockpiling and the contemporary tariff threats, we would must be much more affected person than we have already got been ready for a potential uptick in inflation to now not be a priority.

However the Fed has made it clear this is the reason they haven’t reduce their very own fed funds charge, which has more and more pissed off the Trump administration.

A lot in order that FHFA Director Invoice Pulte issued an announcement about Powell supposedly contemplating an early resignation.

These studies haven’t been substantiated to my data, and can doubtless do nothing to discourage Powell as he waits for extra information to be collected.

That is sort of the irony of the present scenario because the admin stokes inflation issues whereas concurrently asking for charge cuts.

You possibly can’t have all of it, however if you happen to nonetheless need all of it, at the very least present some readability on tariffs and don’t preserve making new threats and elevating the stakes.

Certainly that’s no strategy to get bond merchants to ramp up their purchases and produce yields down.

The excellent news is the 10-year bond yield appears to be again towards the highest of its vary (4.50%) at about 4.43%.

And the longer this goes on, the extra mortgages we’ll originate with larger charges, which sooner or later will likely be ripe for a refinance.

Learn on: Mortgage Charges Are Nonetheless Anticipated to Come Down by the Finish of 2025

(picture: Scouse Smurf)

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and current) house consumers higher navigate the house mortgage course of. Observe me on X for warm takes.